Social Media Addiction Lawsuits Challenge Liability Insurance in 2025

Social Media Addiction Lawsuits Test the Boundaries of Liability Insurance

It began with a chilling story out of Ohio. A 15-year-old girl, once a straight-A student and soccer captain, was discovered by her parents one night after a suicide attempt. In the lawsuit her family later filed, they allege she had been pulled into an endless loop of late-night scrolling, algorithmic nudges, and comparison pressures that left her feeling hopeless.

Her story isn’t isolated. From school districts in California to nonprofits in Florida, the lawsuits piling up against social media giants are anchored in real human suffering. By mid-2025, nearly 2,000 cases have landed in court, and at the center of them all is the question of whether insurers will foot the bill for defending companies accused of designing addiction into their platforms.

When Coverage Meets Conduct

Meta, facing thousands of claims, has turned to its General Liability insurance to cover mounting defense costs. But carriers such as Hartford Casualty Insurance Company are pushing back. Their argument: intentional design choices — like building algorithms to maximize engagement despite known risks — are not accidents, and therefore should not trigger coverage.

That disagreement has already generated its own courtroom battles, with insurers seeking declaratory judgments and Meta filing counterclaims. The industry is watching closely, because whatever line the courts draw will echo far beyond a single defendant.

“We’re watching the definition of coverage for intentional acts being tested in real time, and the precedents could affect liability policies for years to come.”

— Insurance Coverage Attorney

Why General Liability Insurance Matters in Tech

General Liability policies have traditionally been the workhorse of commercial insurance. They protect businesses against claims of bodily injury, property damage, and certain personal injuries. For decades, manufacturers, contractors, and retailers have relied on them to absorb the costs of accidents and unforeseen harm.

But digital platforms present a new puzzle. Are algorithmic design choices more like a product defect, or more like an intentional strategy? And if a harm stems from design, can insurers argue it was no accident at all?

This is the crux of today’s disputes, and the answer will shape how technology firms think about risk transfer.

The Human Side of Liability

Behind the policy language and legal motions are stories that make the stakes clear:

-

A high school district in California claims it had to redirect funds from classroom technology upgrades to mental health counseling as more students struggled with anxiety linked to social media.

-

A nonprofit in Florida reports doubling the size of its crisis hotline team to handle surging calls from teens overwhelmed by online pressures.

-

Families across the country allege that the very features designed to “hook” users contributed to self-harm, depression, and disrupted education.

These aren’t abstract concerns. They are the human backdrop to a coverage debate that may redefine how insurers respond to digital-age liabilities.

What’s at Stake for Insurers

For the insurance industry, these cases are more than just high-profile litigation. They represent a stress test of liability insurance itself. The outcomes could shape how policies are written, priced, and litigated.

Key implications include:

-

Coverage interpretation: Courts will decide how far intentional acts exclusions extend in the digital economy.

-

Underwriting standards: Carriers may tighten terms or introduce specific exclusions for algorithm-driven risks.

-

Policyholder trust: Tech clients may press for clearer commitments if they feel their coverage doesn’t match modern exposures.

“Digital platforms don’t fit neatly into old liability frameworks. We’re being asked to insure against behaviors and harms that weren’t even on the radar when many policy wordings were drafted.”

— Senior Underwriter, Global Carrier

Looking Ahead

With bellwether trials scheduled for late 2025, the insurance industry is bracing for clarity. Insurers are re-evaluating policy language, reassessing reserves, and preparing for ripple effects across liability lines.

For carriers, this is about financial exposure and contract interpretation. For plaintiffs, it’s about accountability and the real costs of digital innovation. And for the insurance market as a whole, it’s a reminder that liability insurance is only as clear as the world it tries to cover.

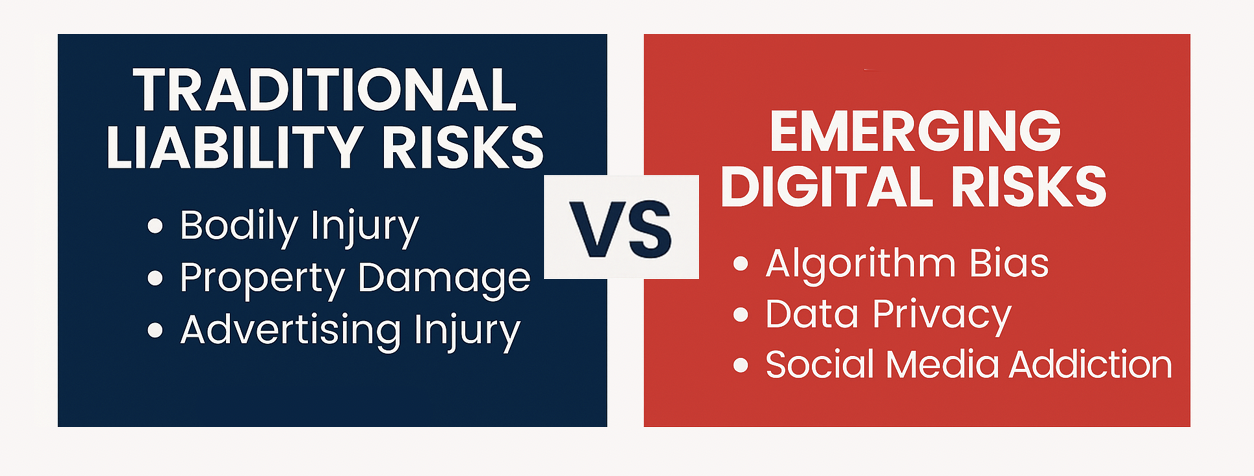

Would you like me to also mock up a small chart showing “Traditional Liability Risks vs. Emerging Digital Risks” to visually reinforce the point about how far the market has shifted?