Rising Auto Insurance Costs Drive Coverage Cuts and Higher Uninsured Rates

Rising Auto Insurance Costs Push Drivers to Cut Coverage—and Some to Drop It Entirely

The U.S. auto insurance landscape is shifting, and not in a way that makes many drivers sleep easier at night. A recent LendingTree survey confirms what many in the industry already suspected: rising premiums are forcing tough decisions.

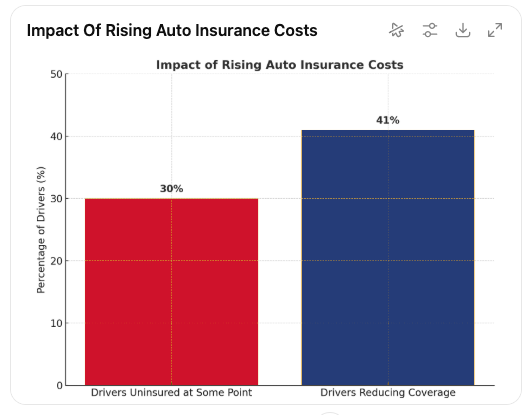

Nearly 30% of drivers admit they’ve driven uninsured at some point, largely because they couldn’t keep up with the cost of coverage. That’s not just a personal risk, it’s a systemic one that ripples through the entire insurance ecosystem.

“When premiums climb faster than paychecks, drivers start making difficult tradeoffs—some with long-term financial consequences.”

Coverage Cuts on the Rise

The survey highlights another concerning trend: 41% of insured drivers are reducing their coverage. Many are opting for liability-only policies. For some, it feels like the only way to stay insured at all. But as industry veterans know, this shift increases exposure to loss, and heightens the stakes when an accident occurs.

States such as Florida, Mississippi, Michigan, New Mexico, Tennessee, and Washington consistently report higher rates of uninsured motorists. In these regions, insurers, regulators, and policymakers face a delicate balancing act between affordability and maintaining a stable risk pool.

How Consumers Are Coping

Beyond insurance adjustments, households are tightening their belts in other ways. To keep coverage active, many drivers are trimming their personal budgets. The survey found that more than half of respondents cut back on everyday discretionary spending.

Here’s where the sacrifices are showing up most:

-

Dining out less often

-

Canceling or pausing streaming subscriptions

-

Reducing gym or wellness memberships

“People are willing to cut Friday pizza nights or Netflix binges—but they can’t cut car insurance entirely without risking far more.”

This reallocation underscores how central insurance is to household stability. Still, the fact that some families are trading essentials for coverage signals a growing affordability challenge.

What This Means for the Industry

For insurers, the takeaway is clear: price sensitivity has reached a boiling point. Consumers aren’t just shopping around; they’re restructuring their entire budgets—or, in some cases, abandoning coverage altogether.

This dynamic opens up critical conversations for the industry:

-

How can insurers, regulators, and policymakers collaborate to ease affordability pressures without destabilizing underwriting fundamentals?

-

Where can innovation—usage-based insurance, digital claims management, AI-driven risk modeling—deliver efficiency and cost savings that trickle down to premiums?

-

What new products or micro-coverage options could keep customers in the risk pool, even when times are tight?

Looking Ahead

The affordability gap in auto insurance isn’t just a consumer issue, it’s an industry-wide challenge that calls for both creativity and compassion. Insurers that step into this moment with flexibility and customer-first solutions will not only preserve market share but also strengthen long-term trust.

Because when coverage becomes a luxury instead of a necessity, the entire system is at risk.