The Medicare Form That Could Save Eligible Retirees Hundreds Each Year

For Medicare clients, Form SSA-44 can turn a confusing premium increase into a practical planning conversation.

Many retirees are surprised when their Medicare Part B premium is based on income from two years ago instead of what they are earning today. That timing can create a painful mismatch for clients who recently retired, lost a spouse, reduced work, or experienced another qualifying income change.

For insurance agents, agencies, and carriers, this is more than a Medicare billing detail. It is a client retention issue, a planning opportunity, and a reminder that Medicare conversations often overlap with retirement income, tax timing, and household transitions.

Why IRMAA Creates Confusion

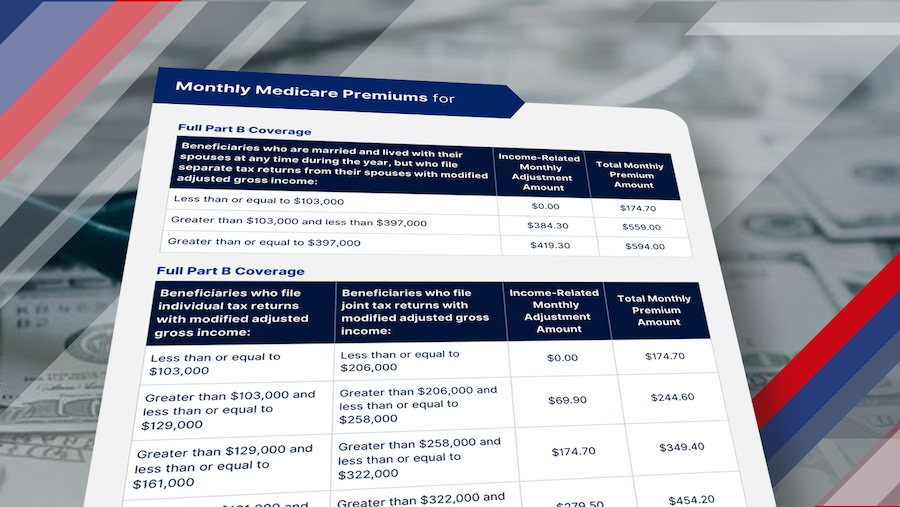

The Income-Related Monthly Adjustment Amount, commonly called IRMAA, is an added charge for higher-income Medicare beneficiaries enrolled in Part B and Part D. Social Security generally calculates it using modified adjusted gross income from the tax return filed two years earlier.

That two-year lookback can make sense administratively, but it often frustrates retirees. A client who had strong earnings in 2024 may no longer have that same income in 2026. Yet their Medicare premium may still reflect the higher-income year unless they qualify for relief.

“If you've had a life-changing event that reduced your household income, you can ask to lower the additional amount you'll pay for Medicare Part B and Part D.”

Attribution: Social Security Administration

What Form SSA-44 Actually Does

Form SSA-44 allows eligible Medicare beneficiaries to ask Social Security to use a more recent income year, or an estimated current-year income, when calculating IRMAA. In plain English, it gives clients a way to say, “My old tax return no longer reflects my real household income.”

This matters because the difference can be meaningful. In 2026, the standard Part B premium is $202.90 per month. A beneficiary in the first IRMAA tier pays $284.10 per month for Part B, plus a Part D surcharge. For a married couple, that difference can quickly become a four-figure annual expense.

The Planning Opportunity for Agents

Agents do not need to provide tax or legal advice to add value here. The practical role is helping clients recognize when a Medicare premium increase may be tied to an outdated income year and encouraging them to contact Social Security, their tax professional, or a financial advisor when appropriate.

That small guidance point can strengthen trust during a moment when many clients feel confused, overcharged, or unsupported.

The Events That May Qualify

Form SSA-44 is not a general appeal for every income spike. It is designed for specific life-changing events that reduce income. That distinction is important because many clients assume any drop in income should qualify.

- Work stoppage: Client retires or stops working.

- Work reduction: Client moves to fewer hours or reduced earnings.

- Death of spouse: Household income and filing status may change.

- Marriage or divorce: Household income calculation may shift.

- Loss of pension income: Certain recurring income ends or declines.

- Loss of income-producing property: Income falls because of qualifying property loss.

- Employer settlement payment: A prior employer-related payment affected income.

The most common client-facing scenarios are retirement, reduced work, and the death of a spouse. These are also the moments when clients are most likely to need help understanding why their Medicare costs changed.

Where Clients Often Get It Wrong

Not every income increase can be reversed through SSA-44. Voluntary financial decisions, including Roth conversions, large taxable withdrawals, or selling a home at a gain, generally do not qualify as life-changing events for IRMAA relief.

That creates an important planning message. Clients may be able to reduce an IRMAA charge after retirement or another qualifying life change, but they usually cannot use SSA-44 simply because a tax-planning move created temporary income.

“To decide your IRMAA, we asked the Internal Revenue Service about your adjusted gross income, tax-exempt interest income, and filing status from your tax return.”

Attribution: Social Security Administration, Form SSA-44

A Simple Way to Explain the Difference

The easiest client explanation is this: SSA-44 is meant for income that changed because life changed, not income that changed because the client chose to create taxable income.

| Situation | Likely Treatment |

|---|---|

| Retirement Work income stops or declines |

May qualify Use SSA-44 for review |

| Death of spouse Household income changes materially |

May qualify Documentation is typically required |

| Roth conversion Voluntary taxable income event |

Usually does not qualify IRMAA may remain |

Why This Matters for Medicare Retention

IRMAA does not change the value of a Medicare Supplement, Medicare Advantage, or Part D recommendation, but it can affect how clients feel about their total Medicare costs. When a retiree sees a larger-than-expected premium, they may blame the plan, the agent, or Medicare generally.

That is why proactive education matters. An agent who can explain the difference between a plan premium and an income-related surcharge helps reduce confusion before it becomes dissatisfaction.

The Carrier Angle

For carriers, IRMAA confusion can influence member experience even when the surcharge is outside the carrier’s control. Clients may not separate government-assessed charges from plan costs, especially when premiums, Social Security deductions, and Part D billing overlap.

Clearer field education can help agents handle those conversations accurately and keep clients focused on coverage, benefits, network fit, drug costs, and long-term plan suitability.

The Client Conversation Agents Should Be Having

The best time to discuss SSA-44 is when a client is transitioning into retirement, reviewing Medicare costs, or questioning a premium increase. Agents can ask whether the client’s current income is substantially lower than the tax year Medicare used to calculate the surcharge.

From there, the agent can explain that Social Security, not the insurance carrier, determines IRMAA. The client may need to submit Form SSA-44, provide documentation of the qualifying event, and estimate current or future income.

This is also a good moment to remind clients that tax professionals and financial advisors should be involved before major income decisions such as Roth conversions, capital gains, or large retirement withdrawals.

A Small Form With a Big Service Impact

Form SSA-44 is not the answer for every Medicare premium complaint, but it can be highly valuable for the right client. Retirement, reduced work, marital changes, and the death of a spouse can all create situations where the old income lookback no longer tells the full story.

For insurance professionals, the takeaway is practical. When clients are surprised by higher Medicare costs, do not stop at the plan premium. Ask whether IRMAA is involved, whether the income year still reflects the client’s reality, and whether a qualifying life-changing event may justify a review.

That kind of guidance turns a confusing bill into a stronger advisory conversation, and it gives clients one more reason to view their agent as a trusted Medicare resource.