California’s Insurance Crisis Is Becoming America’s Insurance Crisis

California’s insurance commissioner race has become far more than a political contest. It is now a high-profile test case for how regulators, insurers, agents, and consumers will navigate the growing challenge of insurance availability in an era of rising catastrophe risk.

For insurance professionals across the country, what happens in California matters. While the headlines focus on wildfire exposure, FAIR Plan growth, and carriers pulling back from certain markets, the underlying issues extend well beyond state lines. From hurricane-prone communities along the Gulf Coast to tornado corridors in the Midwest and coastal regions facing increasing storm losses, the same pressures are reshaping insurance markets nationwide.

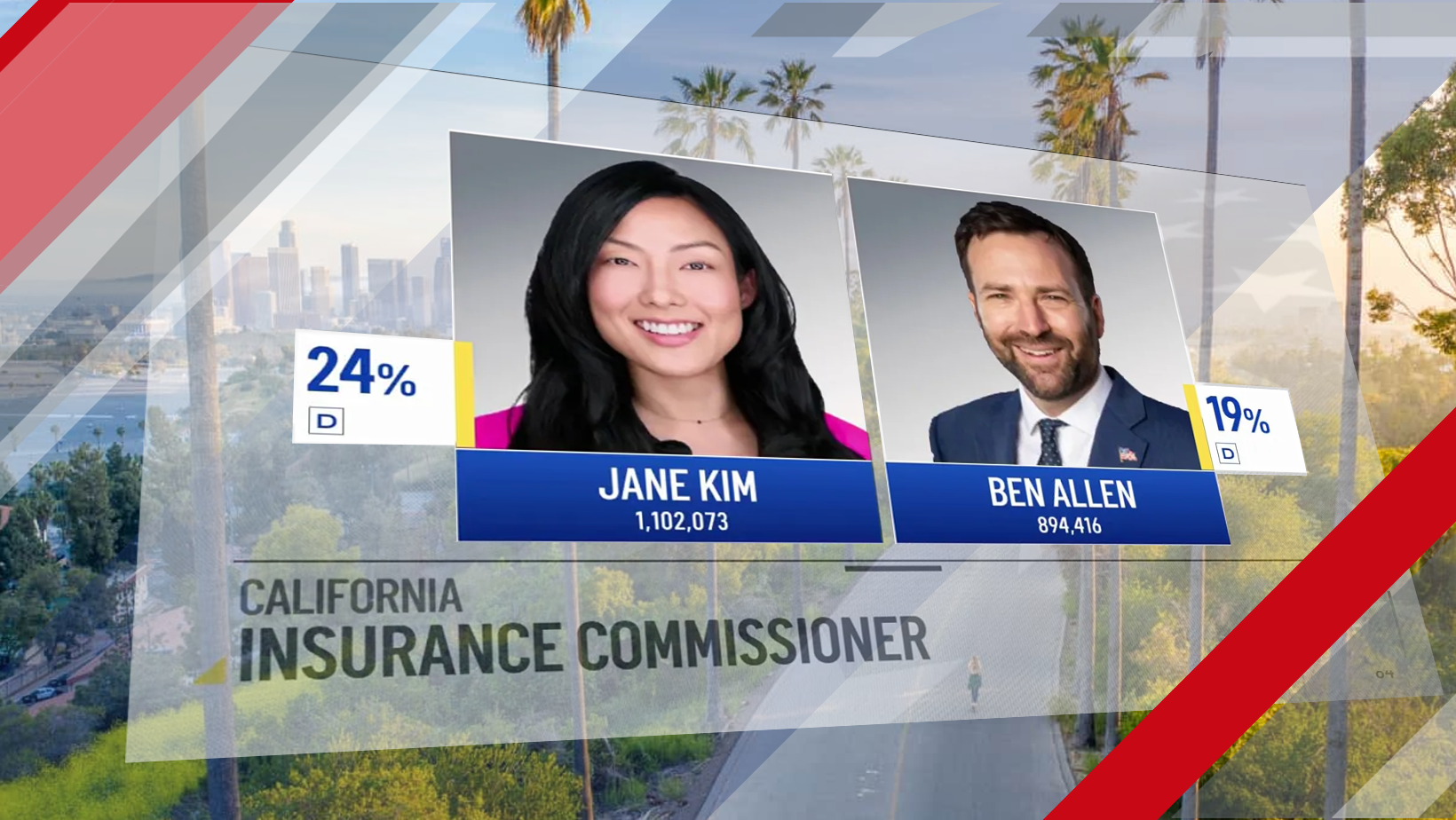

As voters selected California’s next insurance commissioner, industry stakeholders were watching closely. The outcome could influence how one of the nation’s largest insurance markets addresses affordability, availability, consumer protection, and carrier profitability in the years ahead.

Why This Election Drew National Attention

California's insurance commissioner oversees one of the most complex insurance environments in the United States. The position affects regulatory policy, rate approvals, consumer complaints, market conduct, and insurer participation across the state.

What makes this race particularly significant is the backdrop against which it unfolded. In recent years, homeowners throughout California have experienced non-renewals, reduced carrier options, increasing premiums, and growing dependence on the state's FAIR Plan. Many residents found themselves scrambling for coverage after insurers reevaluated wildfire exposure and adjusted their appetite for risk.

"The challenge is no longer simply affordability. In many areas, consumers are struggling to find coverage at all."

Industry market observers

That shift has transformed insurance from a routine household expense into a major public policy issue, placing extraordinary attention on regulators and their approach to balancing consumer interests with market realities.

The Coverage Crisis Behind the Headlines

California's situation did not emerge overnight. A combination of factors has contributed to the current market strain.

Wildfire losses have generated billions of dollars in insured damage over the past decade. At the same time, rebuilding costs have surged due to inflation, labor shortages, and rising construction expenses. Reinsurance costs have also increased substantially, affecting insurers across the country.

Many carriers argue that traditional pricing models and regulatory frameworks have struggled to keep pace with these rapidly changing risk conditions. As a result, some insurers reduced new business activity, limited coverage in higher-risk areas, or exited portions of the market altogether.

Consumers, meanwhile, have faced difficult choices as coverage options narrowed and premiums increased.

The Growing Role of the FAIR Plan

The California FAIR Plan was originally designed as a safety net for property owners unable to obtain coverage through the traditional market. Today, it has become a central part of the state's insurance conversation.

Enrollment has expanded dramatically as more homeowners seek last-resort coverage options. While the FAIR Plan serves an important purpose, many industry experts view its rapid growth as a warning sign that broader market challenges remain unresolved.

The larger the FAIR Plan becomes, the greater the questions surrounding long-term sustainability, risk concentration, and the role private insurers will play in rebuilding market capacity.

What Agents Across the Country Should Be Watching

Although California's circumstances are unique, many agents are seeing similar patterns emerge in their own markets.

Whether the exposure involves hurricanes, hail, convective storms, flooding, wildfires, or severe weather events, carriers everywhere are reassessing risk and adjusting underwriting strategies.

Agents can expect several trends to continue:

- Availability: More selective underwriting in catastrophe-prone regions.

- Pricing: Continued pressure on premiums as carriers respond to loss trends.

- Education: Greater need to explain coverage changes and market conditions to clients.

- Replacement Costs: More scrutiny of valuation accuracy and rebuilding assumptions.

- Alternative Markets: Increased reliance on surplus lines and specialty solutions.

For agencies, these developments reinforce the importance of proactive communication. Clients often perceive premium increases as isolated decisions by their insurer, when in reality they frequently reflect broader market forces affecting entire regions.

A National Snapshot of Market Pressures

The issues facing California mirror concerns appearing throughout the country.

| Region | Challenge | Impact |

|---|---|---|

| California Wildfire exposure |

Higher catastrophe frequency and severity concerns |

Reduced carrier appetite in select markets |

| Gulf Coast Hurricane exposure |

Rising storm losses and reinsurance costs |

Premium increases and market contraction |

| Midwest Severe convective storms |

Frequent hail and wind loss activity |

Stricter underwriting and pricing adjustments |

| Coastal States Flood and storm risks |

Growing property exposure near vulnerable areas |

Expanded coverage challenges for homeowners |

The Regulatory Balancing Act

The debate surrounding California's insurance commissioner race highlights a difficult balancing act facing regulators nationwide.

Consumers understandably want affordable coverage and protection from excessive rate increases. Insurers need pricing flexibility to accurately reflect risk and maintain financial stability. Agents often find themselves in the middle, helping clients navigate the consequences of decisions made far above the kitchen table.

The most successful regulatory approaches will likely be those that encourage market participation while maintaining strong consumer protections. Striking that balance remains one of the industry's biggest challenges.

"A healthy insurance market requires both consumer confidence and insurer confidence. Lose either one, and availability becomes increasingly difficult."

Property and casualty industry analysts

What Comes Next

The newly elected California insurance commissioner inherits one of the most difficult jobs in insurance regulation today. Homeowners want more options. Insurers want sustainable market conditions. Agents want stable solutions they can confidently bring to clients.

The decisions made over the next several years will likely influence how other states respond to similar pressures. That is why insurance professionals nationwide are paying attention.

For agents and agencies, the lesson extends far beyond California. The coverage challenges making headlines today are part of a larger transformation affecting property insurance across America. Understanding those changes, communicating them effectively, and helping clients adapt will remain one of the most important roles insurance professionals can play.