ACA Subsidies Crossroads: What Expiration Could Mean for Coverage and the Insurance Market

The Future of ACA Subsidies: A Crossroads for Insurers and Consumers

As the expiration date for the Affordable Care Act’s enhanced premium subsidies approaches, the debate in Washington has intensified. The subsidies, which were expanded during the pandemic to make coverage more affordable, are set to lapse unless Congress acts. For the insurance industry, the stakes are high: the outcome will shape consumer behavior, market stability, and compliance considerations for years to come.

Why This Debate Matters

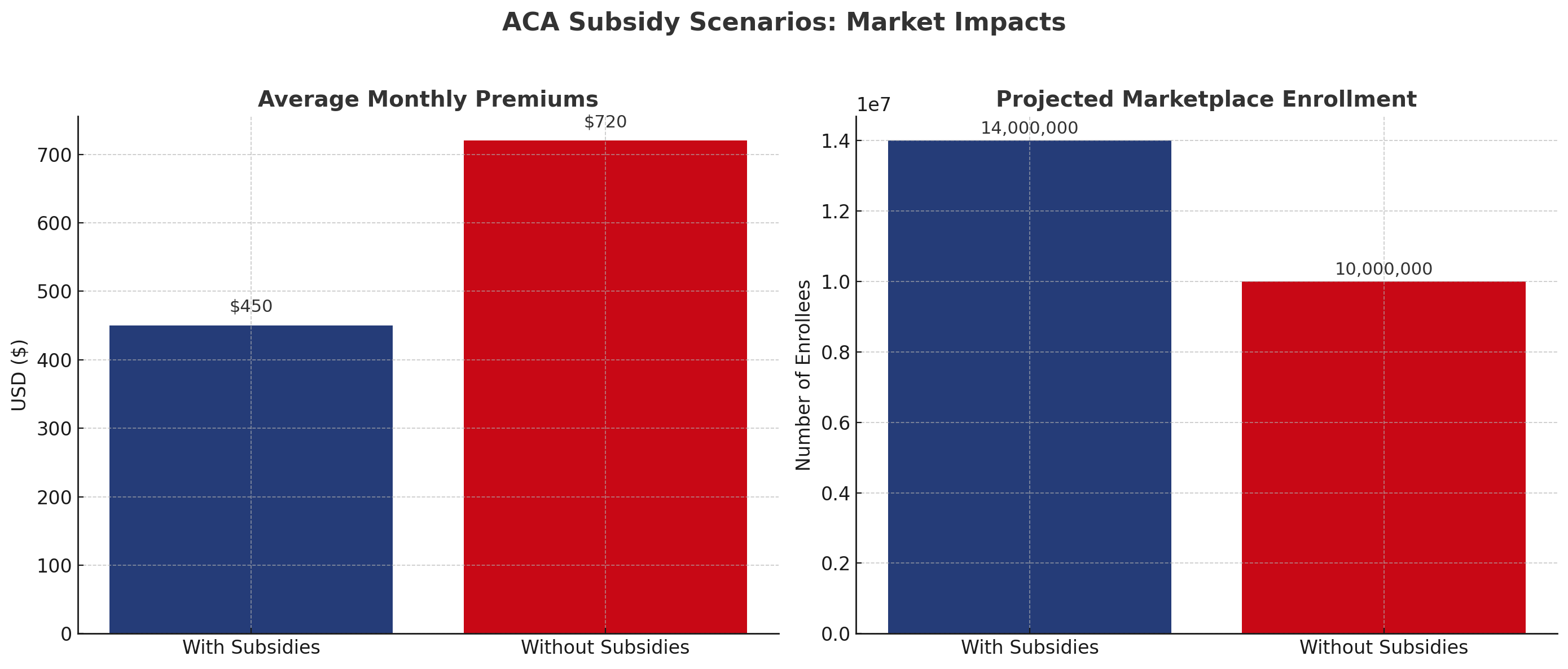

The subsidies directly influence the affordability of individual market coverage. Millions of Americans have benefitted from lower monthly premiums, and insurers have seen stronger enrollment numbers as a result. Without an extension, premium costs could rise sharply, reducing participation in the individual marketplace and potentially destabilizing risk pools.

“Families could see premiums double, and that kind of sticker shock is devastating for affordability.”

— Sen. Jeanne Shaheen (D-NH)

The Democratic Perspective

Democrats argue that making the enhanced subsidies permanent is essential to maintain coverage gains and protect vulnerable populations. They emphasize that the credits help families, small businesses, and older Americans manage rising health care costs. In their view, letting the subsidies expire would undo years of progress in expanding access to affordable insurance.

Beyond affordability, Democrats also highlight the broader health system implications. A reduction in coverage could increase uncompensated care for hospitals, strain community health centers, and ripple across provider networks. For them, the subsidies are not simply a temporary pandemic measure but a foundational tool for health equity.

The Republican Perspective

Republicans have taken a different stance. Many express concern about the long-term fiscal impact of extending subsidies, pointing to the growing federal deficit and rising government spending. They argue that the current structure of the subsidies can disproportionately benefit middle-income households while failing to address underlying health care costs.

“We need to focus on reducing costs, not writing blank checks that increase our national debt.”

— Rep. Jason Smith (R-MO)

Republican lawmakers also emphasize that insurers and consumers alike need more choice and flexibility, not deeper reliance on federal aid. Their proposals often focus on deregulation, expanding health savings accounts, and shifting control back to states to tailor solutions to local markets.

What Insurers Should Watch

For insurance professionals, this is not simply a partisan tug-of-war. The outcome will have tangible effects on rate filings, consumer demand, and market stability. Here are key considerations:

-

If subsidies expire, expect enrollment drops, especially among healthier consumers who are more price sensitive.

-

Premium hikes could accelerate adverse selection, raising loss ratios and pressuring insurers to adjust plan designs.

-

Extended subsidies would support broader participation but may come with tighter oversight and compliance requirements.

-

State regulators may seek to soften shocks through local programs, adding complexity to carrier operations.

A Market Poised for Change

The expiration of ACA subsidies is more than a policy deadline; it is a defining moment for the health insurance marketplace. Democrats frame it as a question of protecting affordability and equity, while Republicans position it as a fiscal responsibility issue and a call for systemic reform. Both perspectives carry weight, and insurers must prepare for either outcome.

“We are at a crossroads. The decision will shape not just policy, but the stability of the insurance market itself.”

— Health Policy Analyst

For the insurance industry, the path forward requires vigilance, scenario planning, and active engagement with regulators. Whether subsidies are extended or allowed to lapse, insurers will be on the front lines of adapting to the next chapter in U.S. health care reform.