Commercial Auto Insurance Posts $4.9B Loss in 2024 Amid Rising Claim Severity

Commercial Auto Insurance Faces $4.9B Loss in 2024: What’s Driving the Trend?

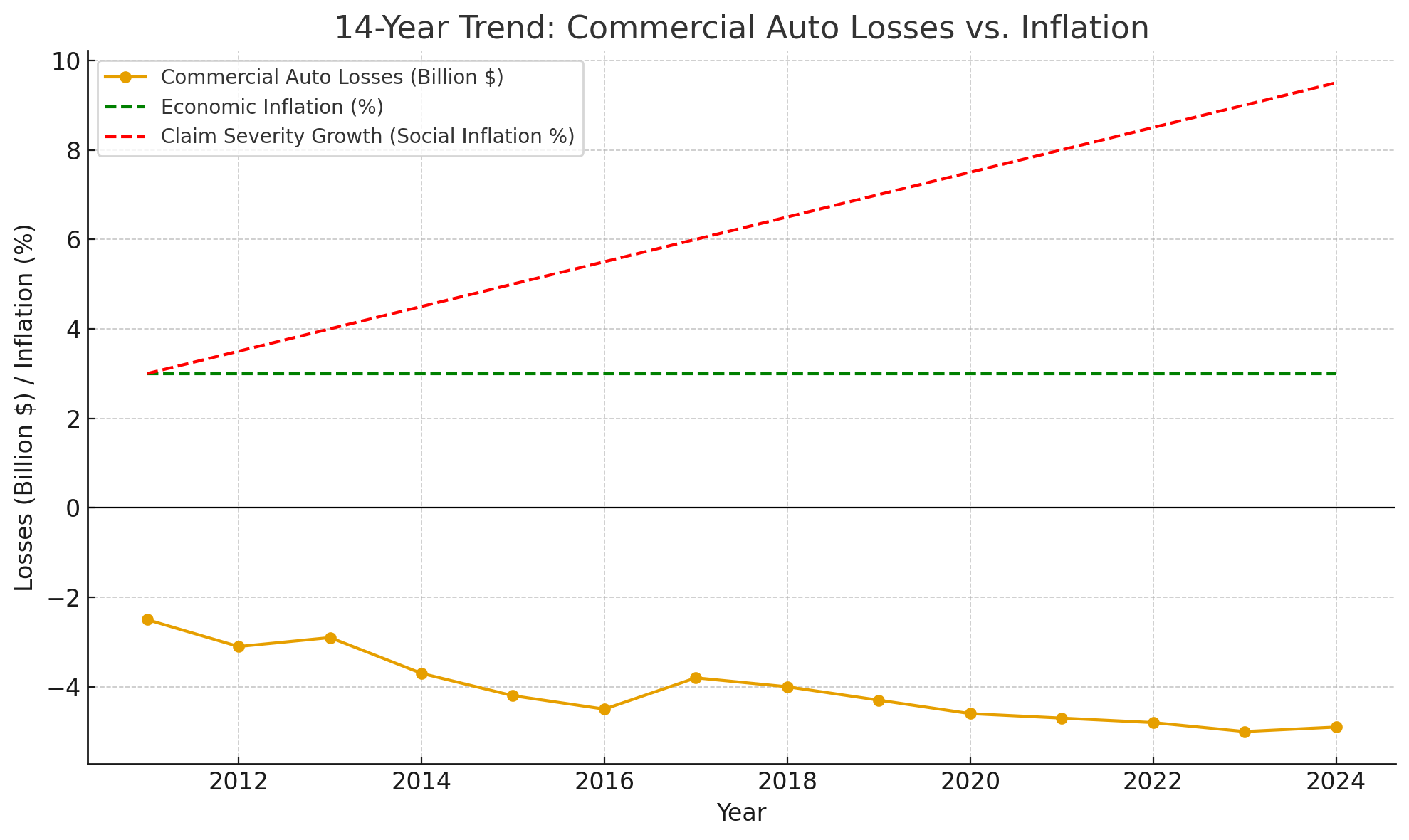

The commercial auto insurance sector is once again grappling with a tough reality. In 2024, the segment posted a staggering $4.9 billion underwriting loss, marking the 14th consecutive year of red ink. For carriers, brokers, and reinsurers alike, this isn’t just a headline. It’s a reflection of deeper systemic pressures reshaping the landscape of commercial auto.

A Long Road of Underperformance

Commercial auto has consistently been one of the most challenging lines to manage. Underwriters are caught between tightening profitability targets and market conditions that seem to shift faster than traditional pricing models can adjust.

At the heart of the issue is the widening gap between economic inflation and what the industry refers to as social inflation. While economic inflation has averaged roughly 3% annually, claim severity in commercial auto has surged about 8% each year. That gap compounds losses quickly, putting sustained pressure on carriers.

“The numbers tell a clear story. It’s not just the cost of repairs or labor—it’s the litigation environment and jury verdicts that are rewriting the rules of risk.”

— Senior Claims Executive, National Carrier

Breaking Down the Drivers

A combination of factors is fueling these losses, and while none are new, the intensity is rising:

-

Litigation and Nuclear Verdicts: Courts continue to deliver outsized judgments against commercial operators, raising average claim costs.

-

Repair Costs: Advancements in vehicle technology, while improving safety, have driven up repair complexity and expense.

-

Medical Inflation: Rising healthcare costs push bodily injury claims higher year over year.

-

Driver Shortages: The industry faces more accidents tied to inexperienced or undertrained drivers filling gaps.

Why Social Inflation Matters More Than Ever

Social inflation has become more than an industry buzzword—it’s now a structural reality. Large jury verdicts, broader definitions of negligence, and evolving societal attitudes toward corporations have created a fertile environment for skyrocketing claims.

“We’ve seen claim settlements that would have been unimaginable a decade ago. That’s the reality we have to underwrite against now.”

— Underwriting Manager, Regional Commercial Auto Insurer

Where Do Insurers Go From Here?

Despite these headwinds, the industry is adapting. Several strategies are on the table:

-

Enhanced Data & Analytics: Insurers are investing in telematics and predictive modeling to more accurately assess driver behavior and risk.

-

Rate Adjustments: Premium increases are inevitable, but balancing affordability for policyholders with the need for profitability remains a delicate act.

-

Claims Management Innovation: Proactive claims handling and alternative dispute resolution are gaining traction to mitigate runaway litigation costs.

-

Partnerships with Insureds: Safety training programs and driver monitoring tools are becoming more integrated into coverage offerings.

The Outlook

The $4.9 billion loss is a stark figure, but it’s also a signal to the industry: the structural forces shaping commercial auto are not short-term anomalies. Insurers must lean on innovation, tighter risk selection, and collaborative approaches with insureds to build resilience.

For many, 2025 may not bring a quick return to profitability. But those carriers who adapt their underwriting discipline, embrace data, and confront social inflation head-on may find themselves ahead when the cycle finally turns.