U.S. P&C Insurance Industry Shows Resilience Amid Rate Declines and Rising Catastrophe Losses

U.S. P&C Insurance Industry Shows Resilience Amid Pressure from Rates and Catastrophes

The U.S. property and casualty (P&C) insurance sector is proving itself remarkably resilient in 2025. Even as global rates decline and catastrophe losses surge, leading carriers continue to demonstrate the ability to adapt, innovate, and grow.

Strength in a Shifting Market

The P&C industry currently ranks within the top 17% of 245 industries tracked by Zacks, reflecting its strong position despite economic uncertainty. While the industry’s annual return of 6.4% lags the S&P 500, select players such as Palomar Holdings, W.R. Berkley, and Axis Capital have consistently outperformed peers.

This divergence highlights a familiar truth for insurance professionals: fundamentals like underwriting discipline, product diversity, and operational agility separate the winners from the rest.

“The market is rewarding those insurers who maintain pricing discipline and embrace innovation, even in the face of headwinds.”

— Industry Analyst, Deloitte Insights

The Rate Landscape: A Turning Point

Global commercial insurance rates fell 4% in the second quarter of 2025, according to Marsh. That marks the fourth straight quarter of decline after seven years of steady increases. The downtrend may unsettle some, but insurers are finding new ways to fuel growth.

Premium expansion is expected to be supported by:

-

Strong policy renewals and retention

-

Expanding agent and broker networks

-

Operational efficiencies that reduce costs

-

Strategic product diversification

Looking ahead, Deloitte projects global gross premiums will surpass $722 billion by 2030.

Catastrophe Losses: A Test of Resilience

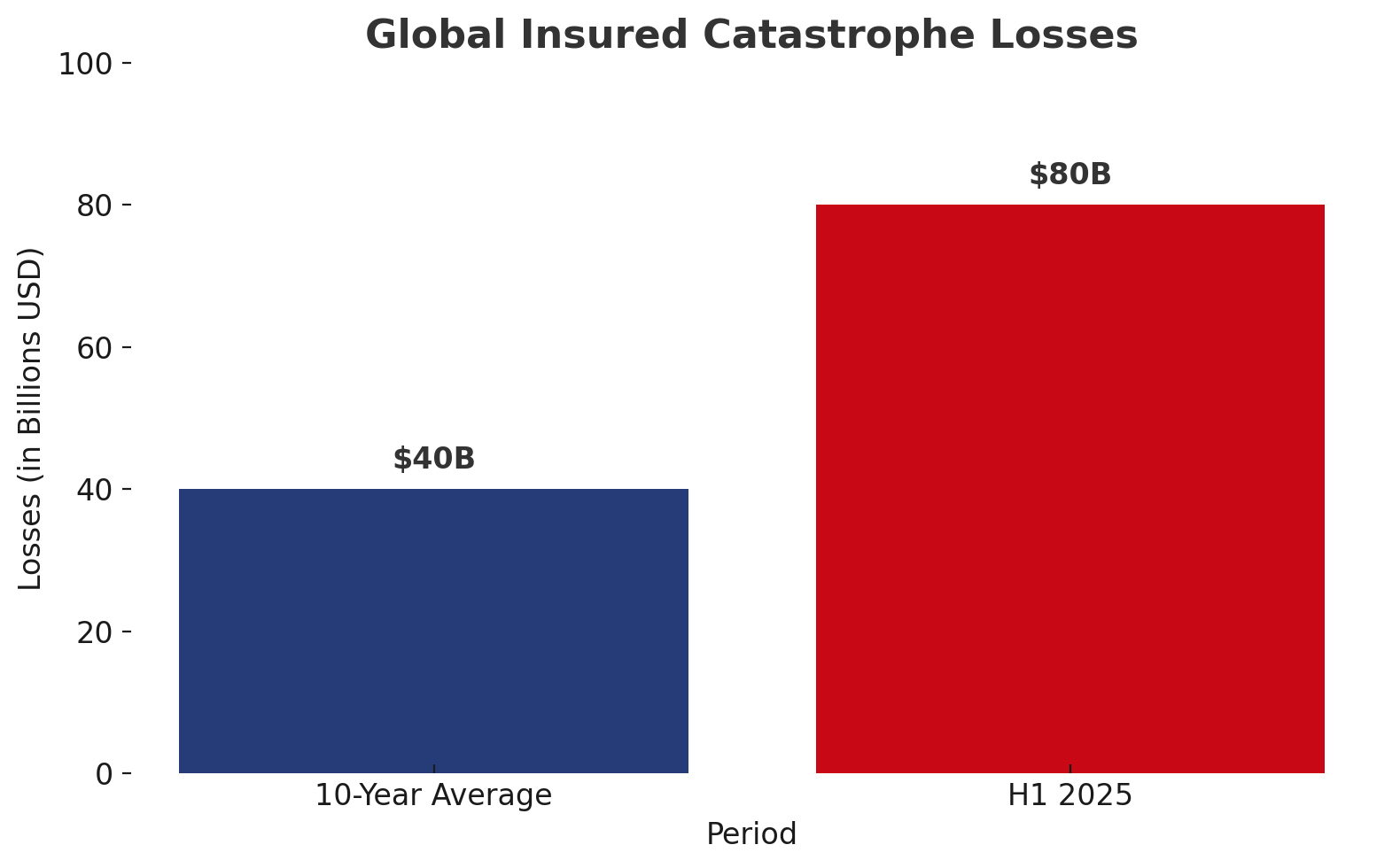

Non-life insurers are facing mounting exposure to severe weather. The first half of 2025 alone brought $80 billion in insured natural disaster losses, nearly double the 10-year average. Convective storms in the U.S. accounted for $31 billion of that total.

Aon estimates total insured catastrophe losses reached $100 billion globally in H1 2025, the second-highest figure ever recorded. When uninsured damages are factored in, the total economic loss climbs to $162 billion.

“The surge in catastrophe claims reinforces the importance of pricing risk appropriately and maintaining strong capital buffers.”

— Chief Risk Officer, Global Reinsurer

The Role of Interest Rates and Technology

The Federal Reserve’s recent rate cut to 4–4.25% offers a mixed bag for insurers. Lower yields reduce reinvestment income potential, but large asset portfolios still provide steady returns that buffer underwriting volatility.

At the same time, technology investment is becoming a defining factor in performance. AI, blockchain, telematics, and advanced analytics are moving from buzzwords to core capabilities. Deloitte forecasts AI-driven insurance premiums could grow to $4.7 billion globally by 2032, with nearly 80% compound annual growth.

Capital Strength and Strategic Moves

Insurers remain well capitalized, and that strength is being deployed strategically. Carriers are pursuing M&A to expand market share and diversify product offerings, while rewarding shareholders through dividends and buybacks. This financial flexibility helps the industry absorb losses while preparing for long-term growth.

Company Spotlights

-

Palomar Holdings (La Jolla, CA): Specializes in catastrophe coverage with a focus on expansion and pricing improvements. Revenue is projected to grow nearly 47% in 2025.

-

W.R. Berkley (Greenwich, CT): A commercial lines powerhouse with steady premium growth and strong returns. EPS is set to climb again in 2026.

-

Axis Capital (Bermuda): Leverages underwriting discipline and global reach to post five-year earnings growth of more than 67%.

The Bottom Line

The P&C insurance sector is navigating a tricky environment of declining rates and escalating catastrophe losses. Yet the industry’s fundamentals remain solid. Strong capital, disciplined underwriting, and rapid adoption of technology are giving insurers the tools to manage volatility and chart a path for growth.

In short, this is not an industry retreating in the face of pressure. It’s an industry evolving.