U.S. Health Insurance Premiums Set for Sharp Increases in 2026

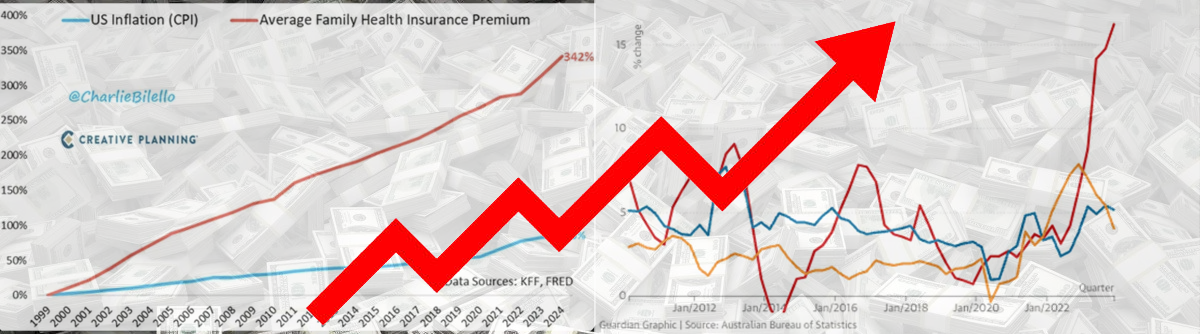

The old refrain “don’t sweat the small stuff” might apply to coffee price spikes—up roughly 48% year-over-year due to climate and tariffs, but not to health insurance. Premiums for employer-sponsored plans have more than quadrupled since 1999, rising over 6% from 2023 to 2024 alone The Washington Post.

Meanwhile, ACA marketplace plans are bracing for even steeper hikes: insurers nationwide have proposed average rate increases of 18%-20% for 2026, marking the largest single-year jump since 2018 Health System TrackerAJMCInvestopedia. Contributing factors include surging medical costs, high-cost specialty drugs, and the looming expiration of enhanced premium tax credits—a change that could lift out-of-pocket costs by up to 75%, effectively pricing millions out of coverage InvestopediaAxiosAmerican Hospital Association.

As Kaiser Family Foundation Health News’ Elisabeth Rosenthal warns, “rising premiums for health insurance…have been trending upward for years and are now rising faster than ever” The Washington Post a stark contrast to the more visible but relatively manageable increases in grocery and gas prices. Business leaders echo the concern: 87% of employers predict that employer-based health insurance will become “unsustainable” within five to ten years The Washington PostKFF.

The potential consequences are profound. Without congressional action to extend federal subsidies, ACA premiums could skyrocket by as much as 75%, resulting in reduced enrollment, sicker risk pools, and a highly unstable market AxiosInvestopediaSan Antonio Express-News. In states like Connecticut, regulators are already reviewing rate requests in the high teens, signaling major upheaval for consumers CT Insider.

This is no small bump in costs it’s a potential tipping point. Whether you serve as an agent, group benefits advisor, or agency owner, this moment demands attention. Employers may need to explore alternative funding strategies, carve out creative benefit designs, and leverage HSAs or telehealth to ease the burden. And individual-market agents should prepare for a surge in consumer outreach during open enrollment, not just questions about premiums, but pressure on budgets and marketplace affordability.