When Life Insurance Becomes Motive: Lessons from An Arkansas Murder Case

Murder, Motive, and a Policy: The Dunigan Case and What It Means for Insurers

In the world of life insurance, most claims represent moments of profound human grief and financial need. But sometimes, a case emerges that shakes the industry with its stark reminder of what’s at stake when life insurance becomes a motive.

That’s precisely what happened in Fayetteville, Arkansas, where 43-year-old Jason Ross Dunigan was convicted of murdering his wife, Amber, in 2021. His motive, prosecutors said, was chillingly clear: profit from a $165,000 life insurance policy and the chance to start fresh with another woman.

A Crime Hidden in Plain Sight

On May 28, 2021, police responded to a call about a woman found dead in her car on a secluded stretch of road near Lake Wedington. Inside was 36-year-old Amber Sue Dunigan, her life cut short by a gunshot wound to the back of the head.

Jason Dunigan was already there when authorities arrived. He told officers he had car trouble earlier and had called his wife to meet him. After driving home alone, he said he became worried when she didn’t follow behind, so he returned with his parents—only to find her dead.

It was a story that seemed plausible on the surface. But beneath it, investigators quickly uncovered a far darker narrative.

The Search History That Told the Story

In court, prosecutors laid out a damning picture of premeditation. For months leading up to Amber’s death, Jason had scoured the internet with a morbid curiosity that pointed directly toward intent.

He researched firearm forensics, ballistics, crime scene investigation, suppressors, DNA testing on shell casings, and even “weirdest ways people have died.” His searches also included snake venom lethality, accidental deaths, choking, overdose methods, and detailed inquiries into when life insurance policies would or would not pay out.

"It only makes sense in the context this defendant was going to kill his wife."

— Dylan Weisenfels, Deputy Prosecutor

For insurance professionals, the sheer breadth of those searches is alarming. It illustrates how perpetrators may attempt to “game” the system by studying policy terms, payout restrictions, and forensic science in hopes of covering their tracks.

A Digital Trail That Couldn’t Be Erased

The state’s case leaned heavily on digital breadcrumbs. Location data from both Amber’s and Jason’s cellphones, navigation logs from their cars, and data from apps painted a detailed timeline.

Jason turned off his phone just after 6 p.m., prosecutors said, and plotted a route to the remote meeting spot. By 8:05 p.m., both phones were at the same location. Amber texted a friend to say she’d found Jason and his car. By 8:09 p.m., her phone went silent forever.

During that narrow window, prosecutors argued, Jason muffled a pistol with one of his neon green work shirts, approached Amber’s car, and shot her through the open driver’s window. The bullet exited her forehead but was never recovered.

He then sped home, reaching 88 mph in a 45 zone, arriving just in time for his home security cameras to mysteriously “resume” recording at 8:25 p.m.—minutes after the system had been deliberately disabled.

Forensics and Fabric

The physical evidence added another layer. Investigators recovered a small piece of neon green fabric from Amber’s wound. Tests later confirmed it matched Jason’s work uniform, supporting the theory that he used it to suppress the gunshot.

Meanwhile, police seized his home surveillance system. Strangely, footage was intact for days before and after the murder, but the exact window of time covering Amber’s death was missing. Jason had accessed the system from his phone multiple times.

A Double Life Uncovered

As investigators dug deeper, they uncovered personal motives intertwined with the financial one. Jason was involved in a sexual relationship with his live-in babysitter, a fact his wife reportedly knew. Another witness testified Jason had complained about delays in collecting his wife’s life insurance, and even speculated that he could pin her death on “a hunter in the area.”

"The defendant in this case did an absolutely evil thing when he murdered his wife to profit from her life insurance and start a life with another woman."

— Brandon Carter, Prosecuting Attorney

Lessons for the Insurance Industry

While the story reads like a crime thriller, it has practical implications for insurers tasked with protecting both policyholders and the integrity of the system.

-

Life insurance as a motive is real: Even modest policies, like the $165,000 payout in this case, can become the centerpiece of deadly plots.

-

Digital evidence is critical: Cars, phones, and apps increasingly provide the timeline that helps insurers and law enforcement validate or dispute claims.

-

Fraud prevention requires cross-disciplinary expertise: Claims teams must often work with forensic analysts, digital investigators, and law enforcement to build the full picture.

-

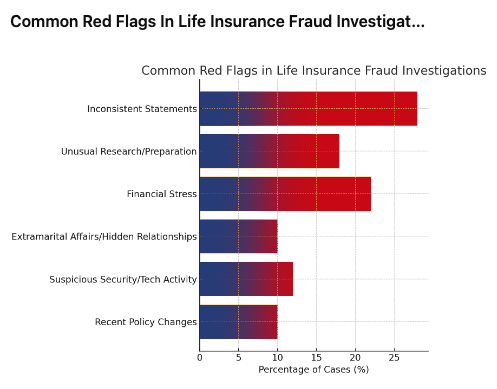

Red flags must be acted upon: Extramarital affairs, unusual financial stress, or obsessive behavior about policies may warrant deeper scrutiny when paired with a suspicious death.

The Bigger Picture

This case is not just about one man’s crime; it’s about the vulnerabilities that exist in a system built on trust. Most policyholders use life insurance for its intended purpose—security and stability. But for a few, like Jason Dunigan, it becomes a deadly temptation.

For insurers, the responsibility lies in thorough, fair investigations that protect beneficiaries without enabling fraud.

"Thorough investigations are not about suspicion, they’re about fairness—ensuring legitimate claims are honored while preventing exploitation of the system."

— Senior Fraud Analyst, National Life Insurers Association

The Dunigan case is a stark reminder that life insurance fraud doesn’t always look like falsified documents or staged accidents. Sometimes, it looks like cold-blooded murder carried out under the guise of financial planning. For the insurance industry, it’s a call to strengthen fraud detection tools, sharpen investigative partnerships, and never underestimate the lengths some will go to for a payout.