Iowa Man Faces Felony Insurance Fraud Charge Over Post-Accident Coverage

When Post-Loss Coverage Becomes a Felony: A Case Study from Iowa

Fraud is a word no insurer ever wants to hear tied to their book of business. Yet, cases like the one unfolding in Iowa remind us how quickly policy manipulation can cross the line into criminal territory.

Recently, a 31-year-old man from Sibley, Iowa, Steven Browning, was charged with felony insurance fraud after attempting to secure coverage after the fact on a damaged vehicle. His situation offers a cautionary tale for both carriers and policyholders.

What Happened

On the day of his automobile accident, Browning reportedly added two vehicles to his Progressive policy, including a 1995 Dodge Ram. He set specific deductible amounts for collision and comprehensive coverage. Less than 24 hours later, he filed a claim for accident damage to that same Dodge Ram—damage investigators say occurred before the truck was insured.

This raised immediate red flags. Presenting false information in this manner fits the definition of insurance fraud, and prosecutors wasted no time moving the case forward. A preliminary hearing is set for October 13 in Osceola County Court. If convicted, Browning could face up to five years in prison.

Why This Matters to Insurers

For carriers, this case illustrates the persistent challenges tied to post-loss coverage attempts. Fraudulent activity like this not only impacts claims ratios but can erode customer trust if left unchecked. The Iowa case underscores how vigilance and investigative rigor help insurers protect their integrity.

“This is exactly the kind of case that highlights why underwriting and claims teams must stay aligned. Fraud prevention begins the moment coverage is requested.”

– Claims Analyst, Midwestern Carrier

Industry Takeaways

While the details of this case are straightforward, the broader implications touch on some of the most pressing issues in auto insurance today:

-

Timing of Coverage Initiation: Backdating or same-day coverage raises natural suspicion during a claim.

-

Claims Pattern Recognition: Quick claim filings immediately after policy updates require heightened scrutiny.

-

Enforcement Visibility: Prosecutions like this show regulators and courts are serious about penalizing fraud.

-

Deterrence Value: Publicized cases serve as reminders to policyholders that fraud is both detectable and punishable.

Looking Ahead

For the industry, Browning’s case is one more example of why detection tools, cross-team communication, and clear customer education remain critical. The message is simple: policies are meant to protect against future risk, not to retroactively cover past losses.

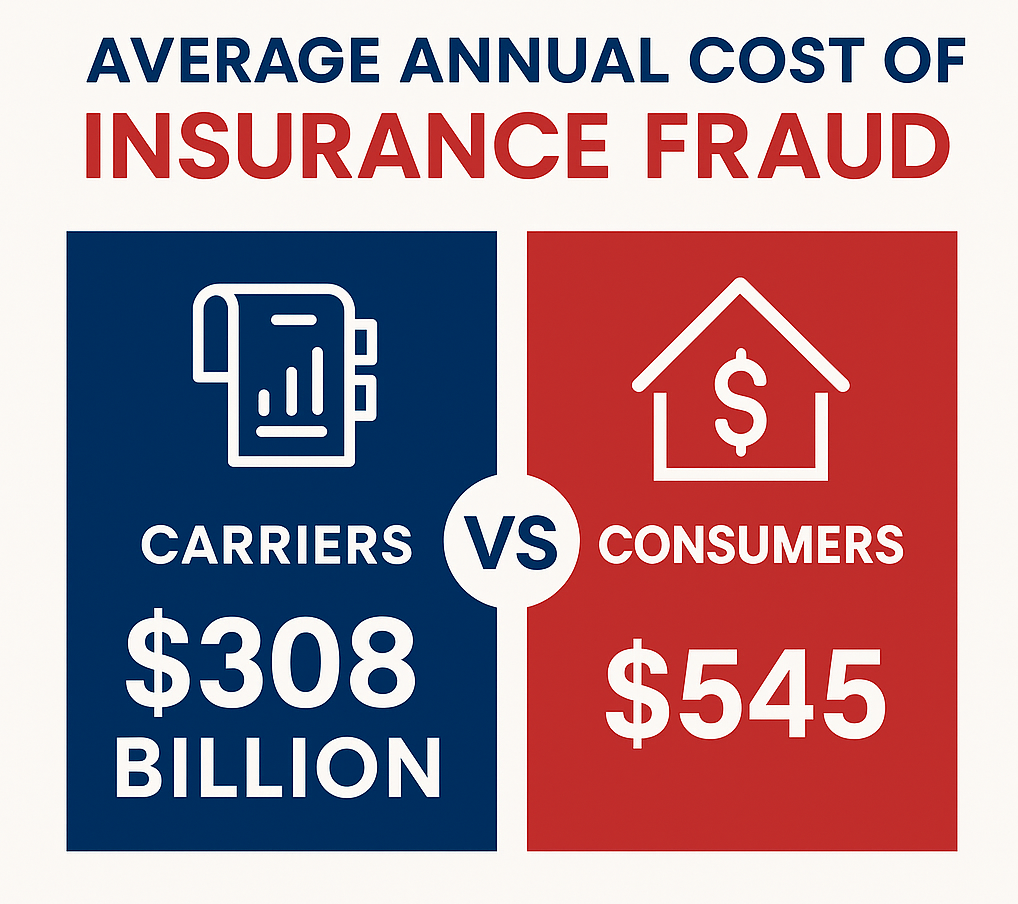

“Insurance fraud may seem small-scale in individual cases, but collectively it costs the industry and honest policyholders billions each year.”

– National Association of Insurance Commissioners Representative

As the trial moves forward, this Iowa story will continue to serve as both a legal test case and a teaching moment. For insurers, it reinforces the need to balance customer service with diligence in spotting inconsistencies. For policyholders, it’s a clear warning: bending the rules can quickly turn into breaking the law.