U.S. Economy Faces 'Quadruple Threat' Impacting Insurance and Market Stability

U.S. Economy Faces a "Quadruple Threat" and Its Ripple Effect on Insurance

The insurance industry has always been closely tied to the health of the broader economy. This fall, the U.S. faces a unique convergence of challenges that could affect both market stability and the way insurers approach risk. Analysts are calling it a "quadruple threat": an auto workers strike, the possibility of a government shutdown, the return of student loan repayments, and rising oil prices. Each factor alone has the power to shake confidence, but together they create an economic pressure cooker with real implications for consumers and insurers alike.

A Consumer Under Pressure

American households have shown remarkable resilience in 2023. Job growth and steady consumer demand have kept the economy from tipping into recession. Yet many families are already stretched thin with higher living costs, reduced savings, and wages that haven’t kept pace with inflation. The new financial headwinds arriving this fall may further test that resilience.

“When consumer wallets are squeezed from multiple directions, we see ripple effects in claims behavior, policy retention, and premium affordability.”

— Senior Insurance Economist

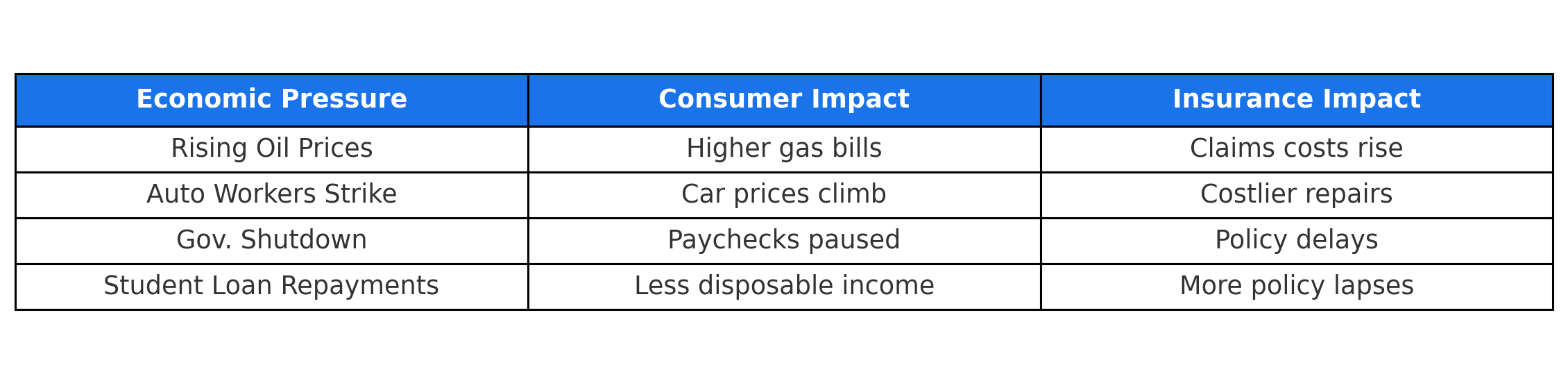

The Four Pressure Points

Here’s a closer look at the economic stressors converging at once:

-

Rising Oil Prices: Households could spend as much as $2,730 on gasoline in 2024. Higher energy costs not only strain budgets but also feed into inflationary pressure across supply chains.

-

Auto Workers Strike: Prolonged labor action threatens vehicle production. Fewer cars rolling off the line means higher prices for both new and used vehicles, which in turn complicates claims severity and replacement costs.

-

Government Shutdown Risk: If Congress fails to pass a budget, up to 800,000 federal employees could be furloughed, leading to reduced consumer spending and increased uncertainty in credit and insurance markets.

-

Student Loan Repayments Resume: More than 44 million Americans will once again make monthly payments, shrinking disposable income and potentially affecting insurance renewals and product uptake.

Implications for Insurers

For insurers, these factors don’t just show up in the macroeconomic data. They manifest directly in customer behavior, claims costs, and investment portfolios. Auto insurers may see increased replacement costs if strikes persist, while health and life insurers could face rising lapse rates as households juggle expenses. Commercial insurers, meanwhile, must monitor how prolonged strikes and supply chain delays affect their corporate clients.

Federal Reserve Chair Jerome Powell has acknowledged the risks posed by this environment. Interest rates remain high as the Fed works to cool inflation without tipping the economy into a recession. But forecasts already suggest growth may slow to 0.8% in 2024, raising the possibility of a harder landing.

“The path to a soft landing is narrowing, and insurers must prepare for both scenarios.”

— Jerome Powell, Federal Reserve Chair

Looking Ahead

For insurers, the takeaway is clear: vigilance and agility are more critical than ever. Underwriting assumptions, risk models, and even product pricing may need to adapt quickly if consumer spending contracts and claims severity rises.

The "quadruple threat" underscores how intertwined economic conditions and insurance markets really are. While no single factor guarantees disruption, their convergence is a test of resilience for both consumers and the industry that protects them.