U.S. Commercial Auto Insurance Posts 14th Year of Underwriting Losses

Commercial Auto Insurance: Fourteen Years in the Red

Commercial auto insurance has now logged an unenviable milestone: fourteen consecutive years of underwriting losses. According to AM Best, the industry has racked up more than $10 billion in losses in just the past two years. The problem isn’t new, but it is deepening, and carriers across the market are grappling with how to regain balance.

“Rate increases have consistently lagged behind loss costs. That gap is what keeps underwriting results negative year after year.”

— AM Best Report

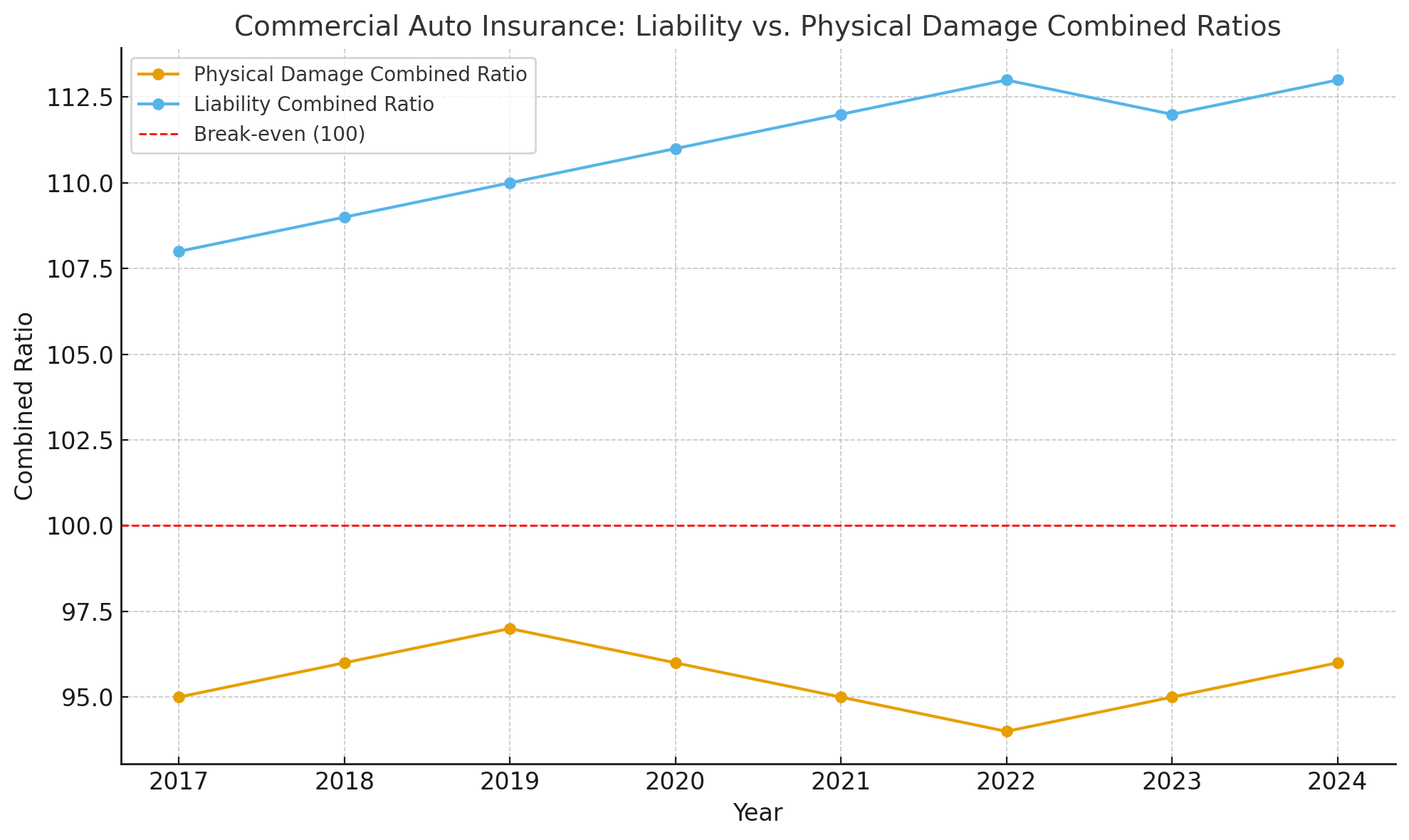

Physical Damage vs. Liability: A Tale of Two Segments

On the surface, not all of commercial auto looks grim. Physical damage insurance has managed to stay profitable, with underwriting profits of roughly $1.5 billion in 2024. Its combined ratio has remained below 100 since 2017.

But the liability side tells a very different story. In 2024, commercial auto liability posted a combined ratio of 113, reflecting steep and persistent underwriting losses. The contrast is striking given that liability coverage is mandatory, while physical damage is optional. Insurers now face the possibility of policyholders scaling back or eliminating physical damage coverage to cut costs, further threatening profitability.

Why Losses Keep Mounting

Industry experts point to several compounding factors:

-

Inflation is driving up repair and replacement costs.

-

Labor shortages have made repairs slower and more expensive.

-

Legal system delays mean claims remain open longer, raising the risk of outsized jury awards.

Prolonged claims are particularly worrisome. AM Best estimates that insurers may be under-reserved by as much as $4 to $5 billion in commercial auto liability. That shortfall puts future profitability at even greater risk.

“The longer claims remain unresolved, the more exposure insurers have to high verdicts. That’s a structural problem we can’t ignore.”

— Industry Analyst

Who’s Winning, Who’s Pulling Back

The competitive dynamics of the commercial auto market are shifting. Progressive remains the dominant player, but even some top-tier carriers are recalibrating strategies. Nationwide, for example, has scaled back premium volume in favor of profitability over growth.

Meanwhile, many insurers have reported combined ratios above 100, a clear sign of underwriting losses. Carriers like Sentry, Chubb, and State Farm are seeing particularly high loss ratios in 2024, adding more pressure to make difficult choices about the future of their commercial auto lines.

Looking Ahead

Commercial auto insurance isn’t disappearing, but the business model is under scrutiny. If losses continue at this pace, more insurers may question whether maintaining a presence in this line of business is worth the strain on their overall portfolios.

The next few years will be pivotal. Insurers that can tighten underwriting discipline, leverage technology for claims management, and price more accurately may finally turn the tide. Until then, commercial auto remains one of the toughest challenges in property/casualty insurance.

Would you like me to create a simple visual chart (e.g., showing liability vs. physical damage combined ratios over time) to go with this article? It could make the divergence between segments more compelling for readers.