U.S. Health Insurance Crisis Highlights Systemic Costs and Reform Challenges

The U.S. Health Insurance Crossroads: Rising Costs, Systemic Strain, and the Road Ahead

Premiums are climbing, subsidies are expiring, and the ripple effects are set to test the stability of the U.S. health insurance system. Employers, insurers, and policymakers all face a moment of reckoning.

“Next year’s projected 9% average increase in employer premiums marks the steepest rise in 15 years.”

Some employers are bracing for hikes above 20% in collective bargaining situations, while individuals on the ACA exchanges may see median increases of 18%. Without extended subsidies, out-of-pocket costs could jump by more than 75%.

Why This Matters for the Industry

Behind the headlines, these shifts aren’t just about rising premiums, they’re about systemic fragility. Federal legislative changes slated for 2027 could alter the balance of Medicaid, employer-sponsored plans, and rural healthcare delivery. For insurers, this could mean higher volatility in membership, sharper churn, and growing demands to innovate coverage models.

“The real challenge isn’t just affordability—it’s maintaining system stability before structural cracks widen.”

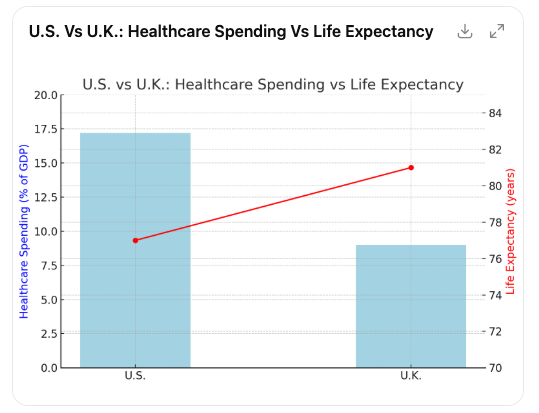

A Global Comparison

The cost differential is staggering. The U.S. spends roughly 17.2% of its GDP on healthcare, while the U.K. spends around 9%. Yet the U.K. consistently delivers higher life expectancy without premiums, copays, or deductibles through its tax-funded NHS.

This gap represents trillions of dollars—funds that, in the U.S., could otherwise be directed toward education, infrastructure, or wage growth. For insurers, this raises the uncomfortable question: is our system sustainable under current models?

Pressures on Employers and Insurers

For carriers and brokers working closely with employer groups, the coming years may look like a perfect storm. Employers face tough choices on benefits design, while insurers must balance profitability with competitive offerings.

Key stress points include:

-

Employer-sponsored coverage strain: Rising premiums pressure employers to shift costs or narrow networks.

-

Medicaid instability: Defunding risks further coverage gaps, especially in rural markets.

-

Federal budget stress: Higher healthcare costs limit investment in other national priorities.

-

Market churn: Rising out-of-pocket costs may drive disenrollment or increased demand for short-term or supplemental products.

The Politics of Reform

The debate is far from settled. Efforts to repeal the ACA have evolved into attempts to weaken its funding pillars. Meanwhile, entrenched stakeholders—the insurance, pharmaceutical, and hospital sectors, make large-scale reforms politically thorny.

But history suggests moments of crisis often spark innovation. Insurers and benefits leaders who anticipate shifts, invest in efficiency, and position themselves as trusted advisors may gain an edge in turbulent times.

Looking Forward

While the system’s challenges are immense, the conversation is shifting from “if” reform will happen to “how.” Carriers, brokers, and benefits professionals should prepare for multiple scenarios: subsidy sunsets, legislative shifts, and competitive pressure from alternative models.

“For the industry, the question isn’t whether costs will rise—it’s how to design solutions that keep coverage accessible and sustainable.”