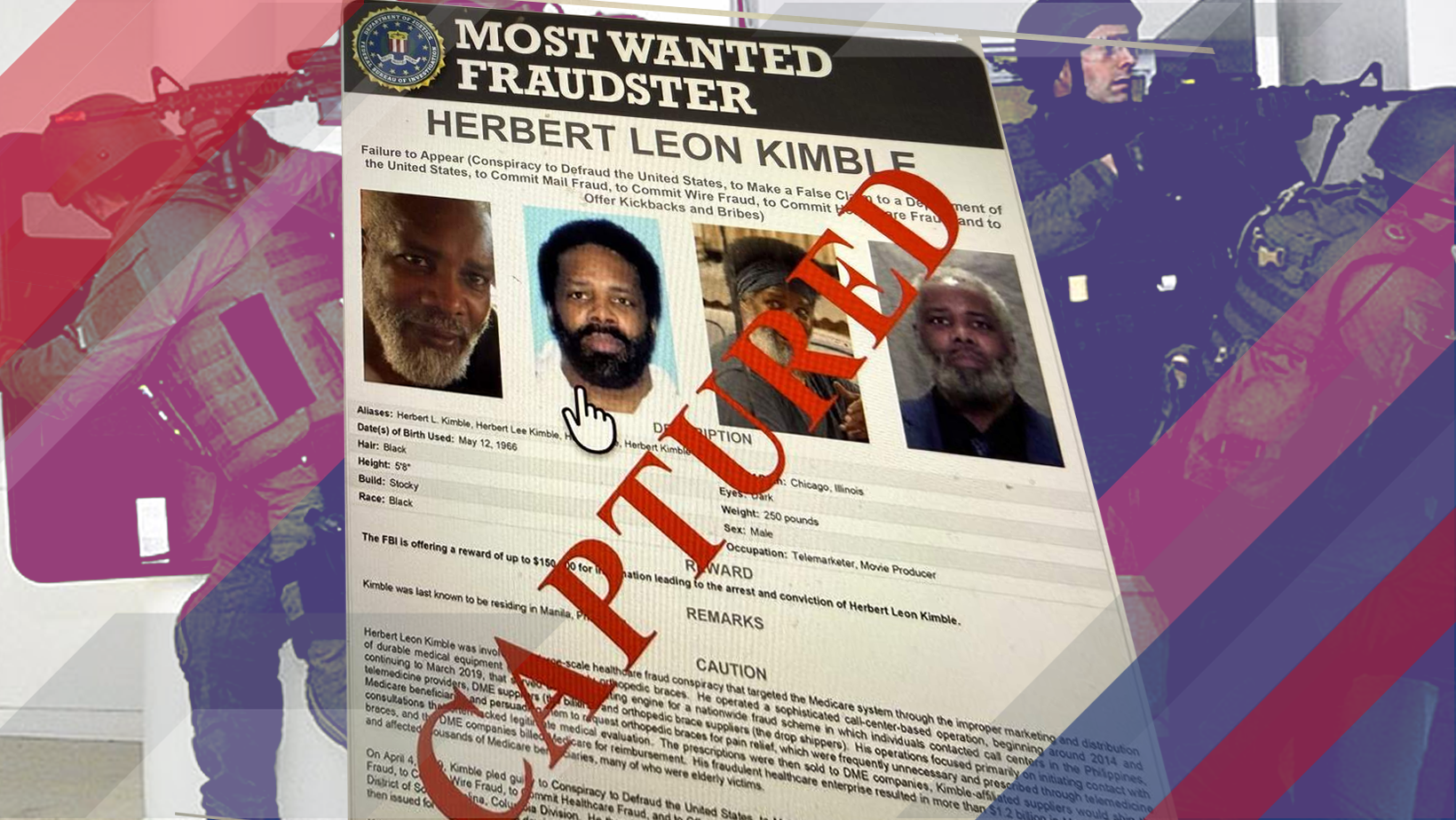

FBI Arrests Herbert Kimble in Massive 1.2 Billon Medicare Fraud Scheme

The arrest of Herbert Leon Kimble in the Philippines gives insurance professionals a timely case study in how modern fraud schemes operate, scale, and cross borders. Kimble had been tied to a large Medicare fraud operation involving medically unnecessary orthopedic braces, call center outreach, kickbacks, and improper billing. For agents, agencies, carriers, MGAs, and compliance teams, the story is less about one fugitive and more about the warning signs that can appear anywhere benefits, referrals, claims, vendors, and vulnerable consumers intersect.

Why This Case Matters To Insurance

Healthcare fraud often sits at the intersection of insurance, consumer protection, provider networks, billing controls, and regulatory enforcement. In this case, federal authorities say the scheme targeted Medicare beneficiaries, many of them elderly, through marketing that pushed orthopedic braces beneficiaries allegedly did not medically need.

That detail should stand out to the insurance industry. Fraudsters rarely rely on one weak point. They combine consumer trust, high-volume outreach, loose referral channels, aggressive billing, and gaps between systems. Once those pieces connect, a scheme can move from isolated abuse to enterprise-level financial harm.

“If you defraud the American people, we will find you and we will bring you to justice.”

Vice President JD Vance

The Fraud Pattern: Simple Pitch, Complex Damage

The alleged mechanics were familiar: call centers, beneficiary outreach, medical equipment, improper referrals, and billing tied to items that may not have been medically necessary. The product category was durable medical equipment, specifically orthopedic braces, but the broader pattern applies across insurance lines.

Fraud often starts with a clean-looking customer interaction. A consumer receives a call, sees an ad, fills out a form, or accepts a “free” service. Behind the scenes, however, the operation may involve questionable lead generation, paid referrals, inflated claims, false documentation, or providers who are not exercising independent medical judgment.

For carriers and agencies, this is why fraud prevention cannot live only inside the claims department. Marketing partners, lead vendors, referral sources, billing workflows, producer conduct, customer complaints, and compliance reviews all matter.

What The Arrest Signals

Kimble had previously pleaded guilty to federal charges that included healthcare fraud and illegal kickbacks, then failed to appear for sentencing in 2024. His arrest in the Philippines, assisted by Philippine authorities, highlights another reality: major fraud cases now move across jurisdictions quickly.

For the insurance sector, international enforcement cooperation is encouraging, but it also underscores the need for prevention. Once a fraud ring has generated massive losses, recovery is difficult. The stronger play is earlier detection, better data sharing, tighter vendor oversight, and faster escalation when patterns appear abnormal.

“Fleeing the United States does not mean you can flee justice.”

Acting Attorney General Todd Blanche

Where Insurance Organizations Should Pay Attention

Fraud schemes like this should prompt insurance leaders to revisit where their own controls may be strongest and weakest. The goal is not to treat every vendor, referral partner, or claim as suspicious. The goal is to recognize that legitimate-looking activity can still create systemic exposure when volume, incentives, and weak oversight collide.

- Lead generation: Watch for high-pressure outreach, vague consent, or unusually high conversion volume.

- Vendor oversight: Review compensation structures, referral relationships, complaint trends, and documentation quality.

- Claims analytics: Flag unusual spikes by product, provider, geography, diagnosis, or beneficiary group.

- Producer conduct: Reinforce training around suitability, misrepresentation, inducements, and vulnerable clients.

- Escalation culture: Make it easy for employees to report patterns before they become losses.

The Consumer Trust Angle

Insurance is built on trust. When fraudsters target older adults, people with health concerns, or consumers who believe something is covered because “Medicare will pay,” they damage more than a public program. They create confusion, frustration, and skepticism that can carry into legitimate insurance conversations.

Agents and agencies are often the front line of that trust. A client may not understand the difference between Medicare, supplemental coverage, a provider, a marketing company, and a third-party vendor. That creates an opportunity for insurance professionals to educate clients in plain language: be cautious with unsolicited calls, question “free” medical equipment offers, protect Medicare numbers, and contact trusted advisors before sharing personal information.

The Bigger Lesson For Carriers And Agencies

The Kimble case reinforces a practical point: fraud prevention is now a strategic capability. It affects claims costs, regulatory exposure, brand reputation, consumer confidence, and operational resilience.

Carriers should continue investing in analytics, special investigation units, provider monitoring, and cross-functional compliance reviews. Agencies should strengthen documentation, training, client education, and referral partner vetting. Everyone in the distribution chain benefits when suspicious patterns are identified early and escalated responsibly.

Large fraud cases make headlines because the numbers are staggering. The real lesson for the insurance industry is quieter but more useful: fraud usually leaves signals before it becomes a billion-dollar case. The organizations best positioned to protect themselves are the ones that know where to look, act quickly, and treat integrity as part of the customer experience.