Turbulence in Private Credit and Its Impact on Insurers

The next major challenge for insurance investors may not be private credit volatility itself, but the growing wall of debt maturities that could reshape portfolio performance across the life, annuity, and reinsurance sectors.

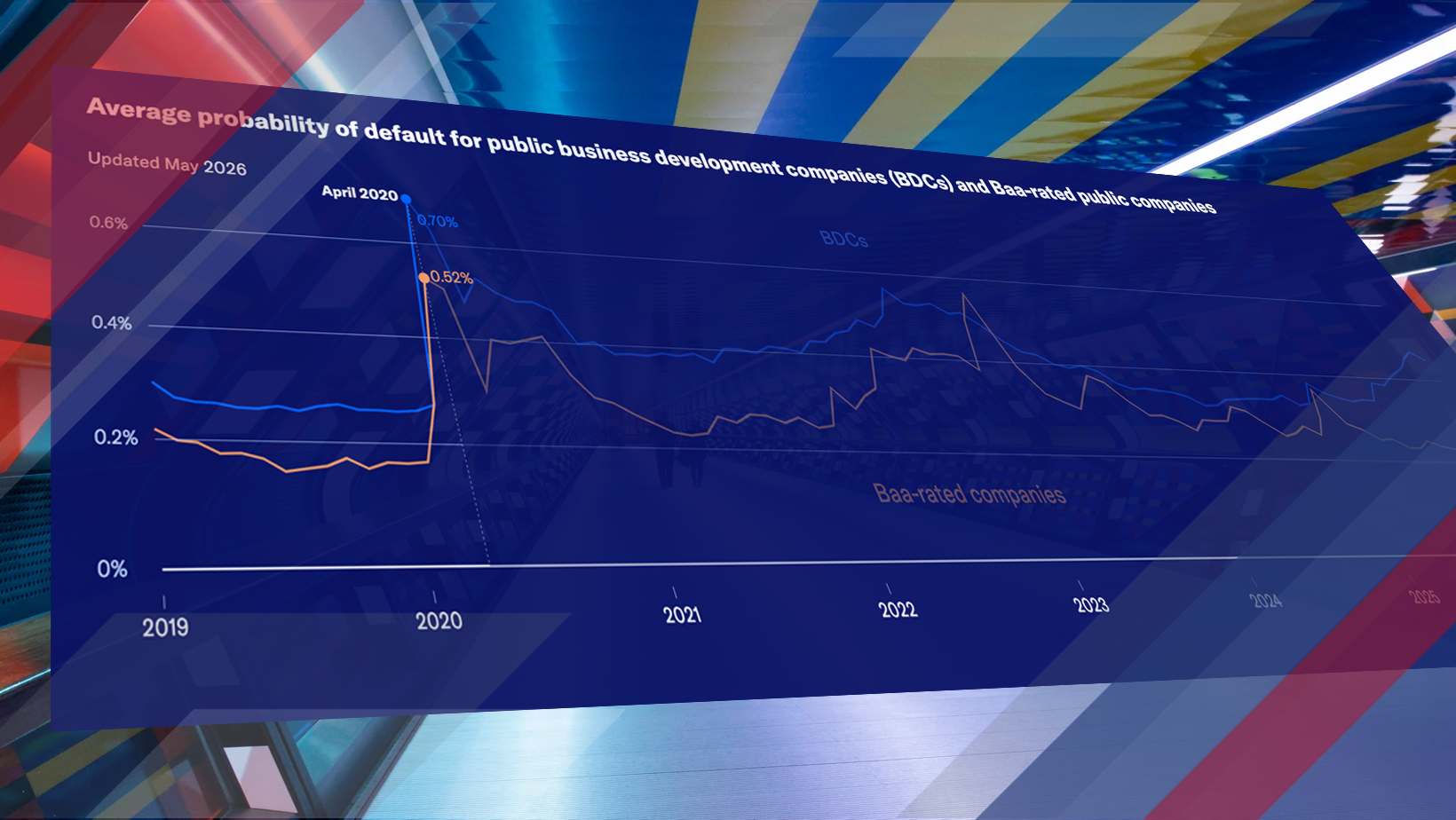

For several years, private credit has been one of the most attractive asset classes for insurance companies seeking higher yields, predictable cash flows, and long-duration investments that align with policyholder obligations. Life insurers, annuity providers, and reinsurers have increasingly allocated capital to private credit strategies as they searched for alternatives to lower-yielding traditional fixed income assets.

While much of the recent conversation has focused on redemption pressures and liquidity concerns within private markets, industry leaders are now highlighting a different and potentially more consequential issue: a significant volume of maturing debt that may face refinancing challenges in a higher-rate environment.

For insurance organizations managing large, long-term liabilities, the implications extend well beyond investment performance. The ability of borrowers to refinance, restructure, or extend existing obligations could influence portfolio valuations, capital requirements, and long-term profitability.

Why Debt Maturities Are Becoming the Central Concern

Private credit markets benefited for years from a favorable environment characterized by low interest rates and abundant liquidity. During that period, many borrowers were able to refinance obligations, extend maturities, or modify loan structures when financial pressures emerged.

Today, that environment looks very different. Higher borrowing costs have increased debt servicing burdens across many industries. As loans approach maturity, borrowers must either refinance at significantly higher rates, contribute additional equity, or face the possibility of distress.

The challenge for insurers is that many of these investments were originally structured with expectations that refinancing markets would remain accessible. If those assumptions prove inaccurate, insurers may encounter valuation pressure on holdings that previously appeared stable.

"In the history of amend-and-pretend, rates have bailed borrowers out. I don't think, in this instance, rates will bail borrowers out."

Mike Paniwozik, Global Head of Structured Credit Investing, Apollo

His comments reflect a growing concern throughout institutional investment circles. The traditional strategy of extending maturities and waiting for lower rates may not be available if borrowing costs remain elevated and economic growth slows.

Why Life Insurers and Annuity Writers Face Unique Exposure

Unlike many asset managers, life insurers and annuity providers typically invest with exceptionally long time horizons. Their portfolios are designed to support liabilities that may extend decades into the future.

This structure has made private credit particularly attractive. The illiquidity premium associated with private assets often provides additional yield compared to publicly traded securities. Those higher returns can improve spreads, support product competitiveness, and strengthen earnings.

However, the same long-duration characteristics that create opportunity can also limit flexibility. When credit conditions deteriorate, insurers cannot always reposition portfolios quickly without affecting asset-liability matching strategies.

As a result, insurance investors must carefully evaluate not only credit quality but also refinancing risk, maturity schedules, covenant protections, and sector-specific economic pressures.

The key question is no longer whether private credit can generate yield. It is whether borrowers can successfully navigate a refinancing environment that remains materially different from the one in which many loans were originally issued.

Insurance Investment Perspective

The Continuing Debate Around the Illiquidity Premium

Even as concerns grow around refinancing risk, major investment firms continue to defend the long-term value proposition of private credit.

Industry leaders argue that investors are appropriately compensated for accepting reduced liquidity. For insurers with predictable liability profiles, holding assets to maturity remains a viable strategy that can unlock meaningful incremental return.

The debate highlights an important distinction for insurance executives. Illiquidity itself is not necessarily the risk. The greater concern emerges when illiquid assets experience unexpected deterioration at a time when market exits become limited or expensive.

This distinction is becoming increasingly important as carriers assess portfolio resilience under multiple economic scenarios, including prolonged higher interest rates, slower growth, and tighter lending standards.

Broader Risk Signals Across the Insurance Industry

The private credit discussion is occurring alongside several other significant risk developments affecting insurers.

One of the most notable involves flood protection. Recent industry analysis points to a substantial gap in uninsured flood exposure, estimated in the hundreds of billions of dollars and potentially approaching one trillion dollars. Despite growing awareness of climate-related risks, many property owners remain underinsured against flood events.

This protection gap creates both challenges and opportunities. Carriers face increasing catastrophe exposure while also identifying potential areas for product innovation and market expansion. As weather-related losses continue to evolve, insurers that can accurately model flood risk may be positioned to serve underserved segments more effectively.

At the same time, changes in public-sector risk tolerance are influencing private markets. Federal entities have demonstrated a growing preference to limit certain exposures, shifting more responsibility to private insurers, reinsurers, and capital providers.

As risk transfer responsibilities migrate toward the private sector, pricing mechanisms are adjusting in real time. Insurers are increasingly relying on advanced analytics, predictive modeling, and dynamic pricing frameworks to maintain profitability while responding to changing risk conditions.

What Insurance Leaders Should Be Monitoring

The convergence of refinancing pressure, catastrophe exposure, and evolving capital market dynamics underscores the importance of disciplined risk management.

For carriers, agencies, and investment professionals, several areas deserve close attention:

- Debt maturity schedules: Identify concentrations of loans approaching refinancing windows.

- Portfolio stress testing: Evaluate performance under prolonged higher-rate scenarios.

- Credit quality trends: Monitor borrower fundamentals and covenant compliance.

- Capital adequacy: Assess potential impacts from valuation adjustments and impairments.

- Emerging protection gaps: Explore opportunities in underserved catastrophe and flood markets.

- Risk transfer pricing: Track how public and private market participation affects underwriting economics.

Insurance Investment Priorities Moving Forward

The insurance industry's growing reliance on sophisticated investment strategies has created meaningful opportunities for enhanced returns. Yet the environment that supported rapid private credit growth is evolving.

Debt maturities, refinancing capacity, and borrower resilience are increasingly becoming the metrics that matter most. While concerns about redemptions and liquidity remain relevant, the larger question centers on whether borrowers can successfully navigate a capital market landscape defined by higher financing costs and greater scrutiny from lenders.

For insurance organizations, success will depend on balancing yield objectives with disciplined risk oversight. Firms that maintain rigorous credit analysis, robust scenario testing, and strong asset-liability management practices will be better positioned to manage uncertainty while continuing to capitalize on opportunities across both investment and underwriting markets.

| Issue | Insurance Impact |

|---|---|

| Debt maturities Refinancing pressure increasing across borrowers |

Portfolio risk Potential valuation pressure and losses |

| Private credit exposure Growing allocation among insurers |

Yield opportunity Enhanced returns with careful oversight |

| Flood protection gap Large uninsured property exposure |

Market opportunity Potential expansion for carriers |