Enrollment Challenges and Premium Surge in ACA for 2026

The Affordable Care Act marketplace is entering one of its most financially challenging periods since its inception, creating serious implications for carriers, agencies, brokers, and consumers alike.

After reaching record enrollment highs in 2025, the ACA market is now showing visible signs of strain as premiums rise sharply and subsidy support declines. Industry analysts, carriers, and policy experts are closely monitoring how affordability pressures may reshape enrollment patterns heading into 2026.

For insurance professionals, the shifting landscape presents both operational challenges and new advisory opportunities. Consumers are becoming increasingly price sensitive, plan migration patterns are accelerating, and retention concerns are growing across nearly every market segment.

Premium Increases Are Reshaping Consumer Behavior

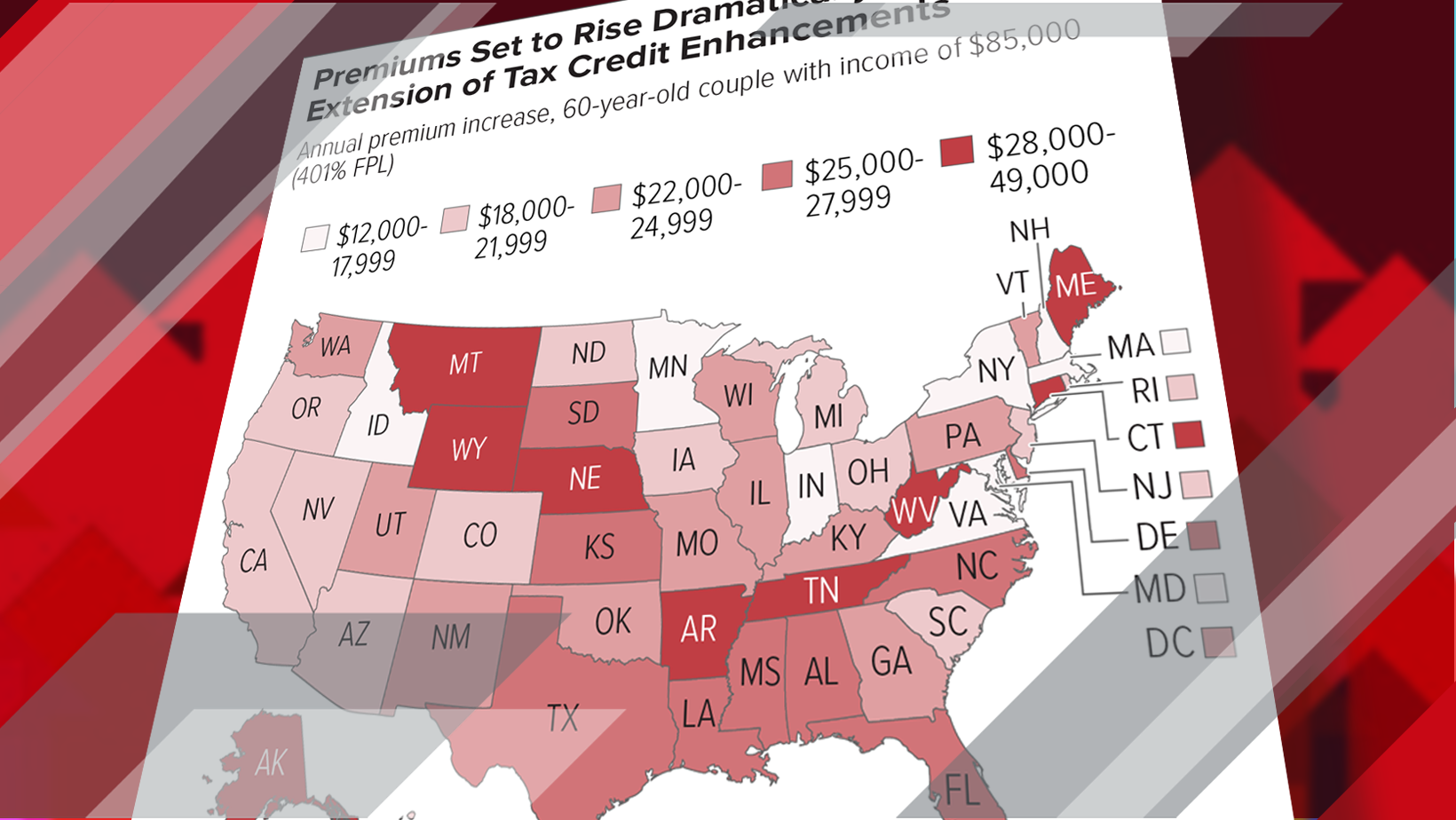

According to recent market analysis from the Kaiser Family Foundation and Wakely Consulting Group, average ACA premiums increased by roughly 26% between 2025 and 2026. In some markets, consumers renewing existing coverage are experiencing premium hikes approaching 100%, particularly among households receiving reduced federal subsidy assistance.

These increases are fundamentally changing how consumers shop for coverage. More individuals are moving toward lower premium bronze-tier plans, despite the higher financial exposure attached to those products.

Bronze plan enrollment climbed significantly, growing from 7.3 million enrollees in 2025 to approximately 9.2 million this year. At the same time, deductibles attached to these plans have surged by 37%, now averaging $3,786 nationally.

“Affordability remains the single biggest driver of enrollment decisions in the ACA marketplace.”

Kaiser Family Foundation

For agencies and brokers, this trend means consumers are increasingly prioritizing monthly affordability over total cost exposure. While bronze plans may preserve enrollment numbers in the short term, higher deductibles can create long-term dissatisfaction when policyholders actually access care.

Coverage Losses Are Accelerating

The industry is already seeing measurable enrollment deterioration. Analysts estimate that more than one million individuals have already dropped ACA coverage because premiums became unaffordable. Projections suggest that figure could rise to four million by the end of the year.

Wakely Consulting Group forecasts that average ACA enrollment in 2026 could decline between 17% and 26% compared to prior-year levels. If those projections hold, the market may experience one of the steepest enrollment pullbacks since the early years of ACA implementation.

The Centers for Medicare & Medicaid Services has also reported concerning payment retention trends. Approximately 21% of federal ACA marketplace enrollees across thirty states failed to make January premium payments, causing early coverage lapses.

By contrast, state-operated marketplaces have demonstrated stronger retention performance, with roughly 92% of enrollees maintaining active coverage. Several states that supplemented reduced federal subsidies with state funding reported comparatively limited enrollment losses.

Why State-Based Exchanges Are Performing Better

The performance gap between federally facilitated exchanges and state-based marketplaces is becoming increasingly important for carriers and agencies operating across multiple jurisdictions.

States that invested in additional financial assistance programs or consumer outreach efforts appear to be stabilizing enrollment more effectively. These programs help offset premium shocks and preserve continuity of coverage among lower-income populations.

In many state-run exchanges, local policy flexibility has allowed regulators to respond more quickly to affordability concerns. Enhanced navigator programs, state-funded subsidies, and targeted retention campaigns have all contributed to stronger payment compliance and lower attrition.

For regional agencies and carriers, this divergence means market performance may vary significantly depending on state policy decisions. Strategic planning now requires far more localized analysis than in previous years.

Regulatory Changes Are Creating Additional Friction

Affordability pressures are not the only issue impacting ACA participation. Recent legislative and administrative changes have introduced new eligibility verification standards and Medicaid-related work requirements that may further reduce enrollment.

These rules are creating additional administrative barriers for lower-income consumers, many of whom already face challenges maintaining continuous coverage.

Several new verification requirements have tightened access to ACA subsidies through special enrollment periods. Consumers who previously relied on year-round enrollment flexibility may now encounter stricter documentation requirements and shorter enrollment windows.

At the same time, the elimination of repayment caps for excess premium tax credits introduces new financial risk for policyholders who underestimate annual income. Consumers who receive larger subsidies than they ultimately qualify for may now face substantial repayment obligations during tax filing season.

“Administrative complexity can discourage participation just as much as premium increases.”

Health policy analysts

For agents and brokers, these regulatory adjustments increase the importance of accurate income forecasting, documentation guidance, and proactive renewal communication.

What This Means for Insurance Agencies and Carriers

The current ACA environment is creating a more consultative role for insurance professionals. Consumers facing rising premiums and higher deductibles are increasingly seeking guidance on balancing affordability with meaningful coverage protection.

Agencies that focus heavily on transactional enrollment may find retention becoming more difficult. Meanwhile, firms that prioritize education, plan comparison support, and ongoing service could strengthen long-term client relationships during this period of uncertainty.

| Trend | Industry Impact |

|---|---|

| Premium Growth Average increases reaching 26% nationally |

Consumer Sensitivity Higher shopping activity and reduced retention |

| Bronze Migration Enrollment rising toward lower-cost plans |

Coverage Exposure Higher deductibles increase member dissatisfaction risks |

| Subsidy Reduction Federal support declining across markets |

Affordability Pressure More consumers exiting the marketplace entirely |

Key Priorities for Insurance Professionals

- Strengthen renewal outreach before premium shock drives attrition

- Educate clients about deductible tradeoffs in lower-tier plans

- Review income estimates carefully to minimize tax credit repayment risks

- Monitor state-level subsidy programs and exchange rule changes

- Prepare service teams for increased enrollment and billing questions

A More Volatile ACA Market Ahead

The ACA marketplace remains a critical coverage source for millions of Americans, but affordability pressures are clearly intensifying. Premium escalation, shrinking subsidy support, regulatory complexity, and tighter enrollment rules are collectively reshaping consumer behavior.

For carriers, agencies, and brokers, the coming enrollment cycles may require greater flexibility, stronger retention strategies, and more proactive client education than ever before.

While enrollment volatility presents immediate challenges, it also reinforces the value of trusted insurance advisors who can help consumers navigate increasingly complicated coverage decisions with clarity and confidence.