Former Deputy Charged with Insurance Fraud and Murder

When Criminal Allegations Collide With Coverage Controls

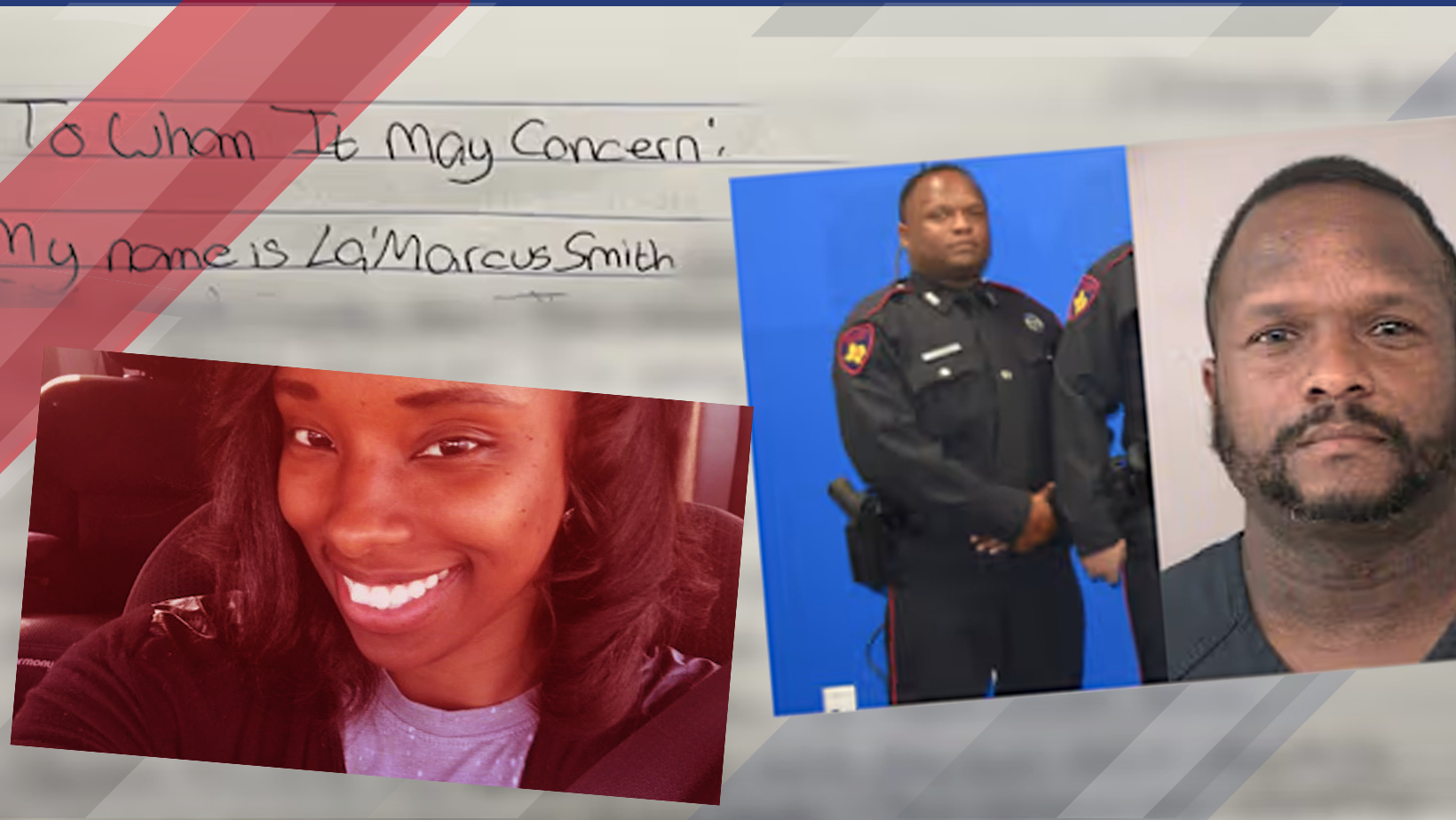

A criminal case unfolding in Texas is drawing attention well beyond the courtroom, particularly among insurers focused on fraud prevention, authentication controls, and reputational risk. Former Harris County Constable Precinct 4 deputy LaMarcus Smith is facing murder charges related to the death of his wife, Laura Smith. Court records also describe separate allegations involving the solicitation of another killing for financial gain and attempted manipulation of a life insurance policy.

For the insurance industry, the case is less about the sensational headlines and more about what it reveals regarding policy servicing vulnerabilities, identity verification, and how quickly criminal intent can intersect with coverage decisions.

“The allegations describe a deliberate effort to exploit insurance processes for personal gain,”

Harris County prosecutors

Alleged Policy Manipulation Raises Familiar Red Flags

Investigators allege that Smith impersonated another individual during a call with an insurer in an effort to alter a life insurance policy. While the criminal proceedings will determine culpability, the scenario itself is a familiar one for insurers. Policy changes requested by phone, particularly beneficiary updates or coverage modifications, remain a common entry point for attempted fraud.

The allegations also highlight how social engineering can bypass controls that appear sufficient on paper. Even experienced professionals can underestimate how convincingly a determined individual may present themselves during routine service interactions.

“Fraud attempts often succeed not because controls are absent, but because they are inconsistently applied,”

Harris County prosecutors

Broader Implications for Insurers

This case arrives at a time when insurers are already reassessing operational risk. Automation, artificial intelligence, and streamlined authorization processes have delivered efficiency gains, but they also demand stronger governance. When authentication protocols lag behind service innovation, the exposure is not limited to financial loss. Public trust and regulatory scrutiny quickly follow high profile failures.

A judicial gag order now limits public disclosure, but the insurance implications are already clear. Cases like this tend to resurface during regulatory exams and internal audits as examples of why robust identity verification is not optional.

Practical Takeaways for Insurance Operations

-

Reinforce multi factor authentication for all policy changes, not just high value transactions

-

Standardize call center verification scripts and require escalation for any deviation

-

Audit beneficiary and ownership changes with post transaction reviews

-

Train service staff to recognize social engineering techniques, even from seemingly credible callers

A Snapshot of Control Points Under Scrutiny

| Process Area | Common Weakness | Risk Exposure |

|---|---|---|

| Policy servicing | Single factor identity checks | Unauthorized changes |

| Call center workflows | Inconsistent escalation | Social engineering success |

| Beneficiary updates | Limited post change review | Financial and legal disputes |

| Compliance oversight | Siloed reporting | Delayed fraud detection |

Trust, Compliance, and the Long View

Laura Smith, an elementary school teacher, was found deceased in her Richmond, Texas home in May 2024. The criminal case continues, and its legal outcome remains unresolved. For insurers, however, the lessons do not depend on a verdict. High profile cases tied to insurance manipulation inevitably shape public perception and regulatory expectations.

The industry has long understood that fraud prevention is not a single control or technology. It is a discipline. As insurers balance efficiency with security, this case serves as a sobering reminder that even routine transactions deserve rigorous attention.